8% Yield And 40% Upside At The Beaten Down Investors Real Estate Trust

The Buy Thesis

Investors Real Estate Trust (NYSE:IRET) has taken it on the chin as the Bakken shale play busted and real estate in the surrounding area suffered. This hardship triggered a portfolio repositioning that is going to leave IRET with a much stronger asset pool. Market pricing suggests further hardship, but a deep dive into company fundamentals shows that it is in the early innings of a substantial recovery. We see 40% upside as the dust settles, revealing IRET’s new and improved portfolio, and a strong 8% yield pays investors until the capital gains can be realized

As the fracking kicked off in the Bakken shale, IRET looked promising with its headquarters in Minot, ND, and a material portion of its properties directly exposed to the economic activity in the area. Oil was valuable, and there were high hopes for the region’s fracking as it began ramping up construction to facilitate operations and importing workers with promises of high wages. At $100 per barrel of oil, the future looked bright.

However, as oil started to tank in late 2014, the region suffered. Its marginal cost per barrel is substantially higher than other parts of the US, so it was among the first to stop drilling and it shut down harder than other oil plays. Much of the economic activity that entered the region suddenly left, but the freshly supplied properties remained. The resulting combination of high supply and recessionary demand caused rampant vacancy across various types of real estate and threatened rent per square foot. IRET had enough exposed properties that it suffered both fundamentally and in market pricing.

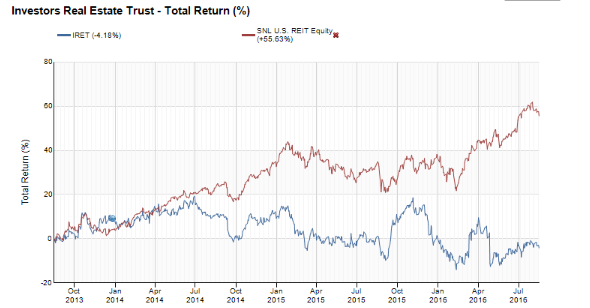

Note the nearly 60% underperformance since the oil bust.

Opportunity through hardship

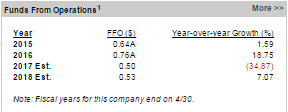

IRET’s troubles are quite visible and easy for the market to price in. Management provided guidance for FY 2017 that was about 30% lower than FY 2016 FFO/share and the Street estimates (shown below) dropped down to $0.50 to match the guidance.

(Data from SNL Financial)

With each downward revision to consensus estimates, IRET’s market price either tanked or failed to increase as the rest of the REITs were soaring. 60% underperformance in market price is easily enough to compensate for a roughly 35% drop in FFO/share. Thus, on a relative basis, IRET got very cheap compared to other REITs.

While management was not without blame, having perhaps gotten overly ambitious during the good years, it has done a good job repositioning IRET for recovery. Focus seems to have been entirely on the troubles with IRET’s repositioning flying under the radar. The quality of IRET’s assets has improved dramatically, which positions it for material growth going forward.

This is the key to our thesis. The market is pricing in the reduced FFO guidance, but it is not pricing in the improved quality. IRET should be trading at a substantially higher multiple.

A new and improved portfolio

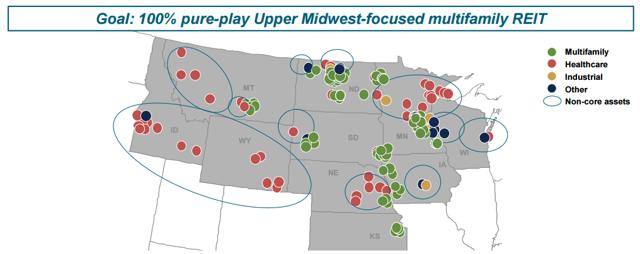

IRET is classified as a diversified REIT with exposure to multifamily, healthcare, industrial, retail and office assets. In its repositioning, it is becoming a pure-play multifamily REIT as announced in its presentation shown below:

It is well on its way to accomplishing the goal, having already disposed of a majority of the office and retail assets.  (Source: IRET)

(Source: IRET)

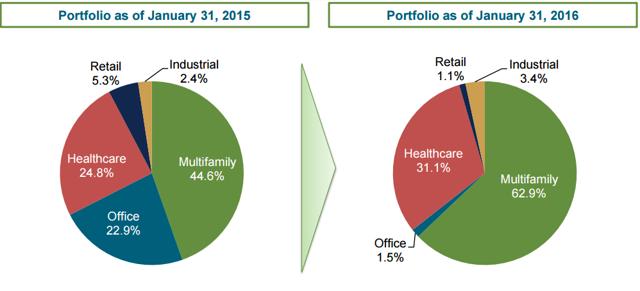

The remaining portfolio is almost entirely multifamily and healthcare, with the healthcare component consisting of MOBs and senior housing. Importantly, both MOBs and senior housing are highly sought-after assets, so IRET should be able to sell these accretively, and we anticipate an average cap rate of 5.5-6% for the senior housing assets and 6-7% for the MOB sale.

As one of the only REITs that participates in the Midwest, it should be able to acquire or develop multifamily properties of good quality at a cap rate near or slightly higher than 6% such that the remaining repositioning should be roughly neutral to FFO/share.

Fundamental outlook

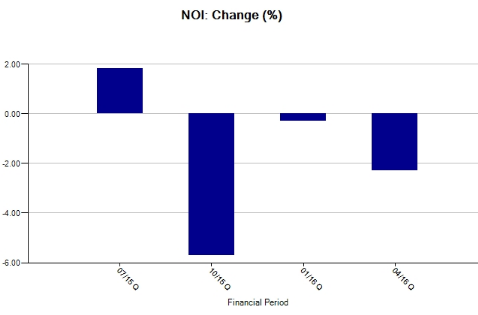

We view the roughly $0.50 FFO/share guidance as a base from which IRET can grow. Much of the negative growth seen in the recent quarters was a delayed result of the shock to the oil field markets. As the existing leases expired, renewal rates were generally lower causing negative SSNOI.

(Data from SNL Financial)

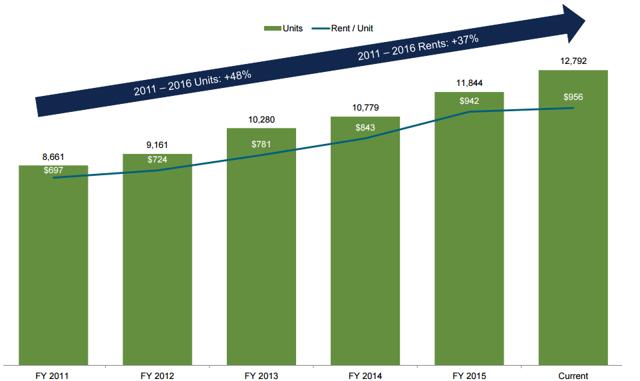

Digging deeper, it seems the negative NOI growth was from the office and industrial sectors with its multifamily properties performing quite well. In the most recent quarter, multifamily SSNOI growth was 4.8% excluding energy impacted markets. This builds on a longer trend of rent growth in its multifamily portfolio.

(Source: IRET)

(Source: IRET)

As IRET’s portfolio is now dominated by multifamily assets, we anticipate its overall SSNOI will trend positive and that will bring the FFO/share with it. Additionally, IRET has a couple developments expected to be delivered in 2017 which should further bolster cash flows. (Source: SNL Financial)

(Source: SNL Financial)

Overall, we estimate IRET to grow at a slow to moderate pace going forward.

Given this outlook, how should IRET be valued?

Asset Valuation

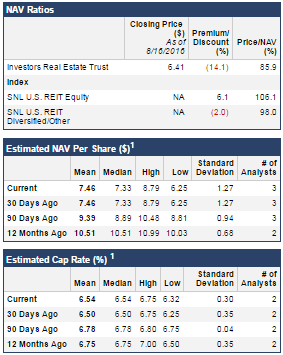

On an NAV basis, IRET is rather cheap at a 14% discount to NAV.

(Data from SNL Financial)

The $7.46 consensus estimate is based on a cap rate of 6.54%, which is fairly conservative. NexPoint Residential Trust (NYSE:NXRT) has recently sold class B multifamily properties at below 6%. IRET’s portfolio has slightly higher rent per unit, so it should arguably have a lower cap rate than NXRT. Thus, IRET is cheap relative to consensus NAV and even cheaper relative to the market cap rate implied NAV for assets of similar quality. At a 6% cap rate, IRET has an NAV of $9.18 based on LTM NOI.

Trading at $6.45, IRET could appreciate over 40% to get to a 6% implied cap rate, which would be reasonable for a multifamily pure-play.

FFO valuation

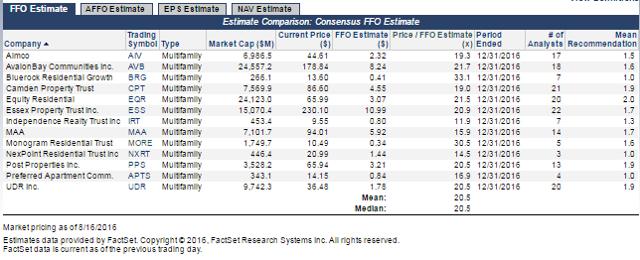

As a company that is fundamentally positioned to grow at a slow to moderate pace (from its reduced base of $0.50 FFO/share), IRET should trade closer to peers. Multifamily REITs in general are expected to grow at a slow to moderate pace, and I would anticipate IRET being in the middle of the pack. However, it does not trade in the middle of the pack with a multiple of just 13X forward FFO as compared to 20X forward FFO for the sector.

(Source: SNL Financial)

(Source: SNL Financial)

Although not traditional, I would actually give a slight bonus to IRET for its Midwestern focus. The Midwest is arguably America’s most stable region with unemployment rates over 100 basis points lower than the national average. Additionally, the slower pace of Midwestern lifestyles promotes longer average stay, resulting in lower churn for IRET than multifamily peers.

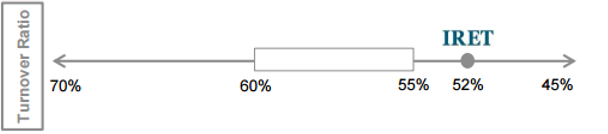

In this case, the blank box above represents the range for the peer set consisting of AIV, APTS, BRG, IRT, MAA, MST and NXRT.

Catalyst: Pure-play-premium

Once IRET completes its sale of the MOB and senior housing portfolios, it will be over 90% multifamily, which will qualify it to be labeled as a pure play and join the multifamily REIT sector. Once it loses the stigmatized “diversified REIT” label, it should experience material multiple expansion. We anticipate it trading closer to 18X 2017 FFO, which would still be a discount to peers. This equates to a $9.00 stock price or roughly 40% upside from where it trades today. This valuation is backed up by the NAV analysis above.

Risks and concerns

While I believe most of the energy-related troubles are behind us, another material shock to oil prices could shut down whatever areas of the Bakken are still operational. Portions of it might be cash flow positive at $40/barrel oil, but certainly not at $25 oil. Such a shock would worsen the outflows of oilfield employees, thereby reducing demand for multifamily units in the area. While IRET has been moving its concentration more heavily to Minnesota, there is still enough of its portfolio in or around the Bakken that it would hurt. Conversely, full recovery of oil prices would reinvigorate the area and bring back the portion of revenues that IRET lost.

IRET has not been stating the cap rate at which its assets are sold. My analysis is based on a market cap rate for properties of the given quality of the given type in the submarket or region. If for whatever reason IRET were getting a bad deal (worse than market rate) in its asset sales, my outlook would have to be shifted down accordingly.

The bottom line

IRET’s portfolio transformation has been overlooked in the wake of its oilfield troubles. Once the dust settles, we believe the market will begin to see that its remaining assets are quite strong. This, along with a demonstration of positive SSNOI growth, should fuel material multiple expansion for a potential 40% capital appreciation.

Disclosure: 2nd Market Capital and its affiliated accounts are long IRET, IRT and NXRT. I am personally long IRET and NXRT. This article is for informational purposes only. It is not a recommendation to buy or sell any security and is strictly the opinion of the writer.

Disclosure: I am/we are long IRET, NXRT, IRT.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.