AzurRx BioPharma Is An Ultra-High-Risk IPO

AzurRx BioPharma (Pending:AZRX) is developing a treatment for pancreatic insufficiency with the scientific backing of European biopharma researchers.

While it has earned Phase 1 clinical trial success for its lead candidate, the hardest part lies ahead, and the company is thinly capitalized for such a significant undertaking.

The financial and scientific hurdles are quite high, too high at this juncture for my taste, so I suggest avoiding this ultra-high-risk biopharma IPO.

Company Background

AzurRx BioPharma has filed for its IPO to sell up to $15 million of its common stock at a target of $7.00 per share.

Currently, at the clinical development stage, AzurRx is a Brooklyn, NY-based company (with scientific operations in France) that is developing recombinant proteins to treat gastrointestinal and microbiome conditions via orally-delivered biologics.

It has two products in its pipeline:

- MS1819 is its lead EPI (exocrine pancreatic insufficiency) candidate and has received the greatest amount of company investment and focus to-date. MS1819 – A potential treatment for pancreatic insufficiency, in-licensed from Laboratoires Mayoly-Spindler.

- AZX1101 – An enzyme designed to help prevent hospital-acquired C. difficile infections.

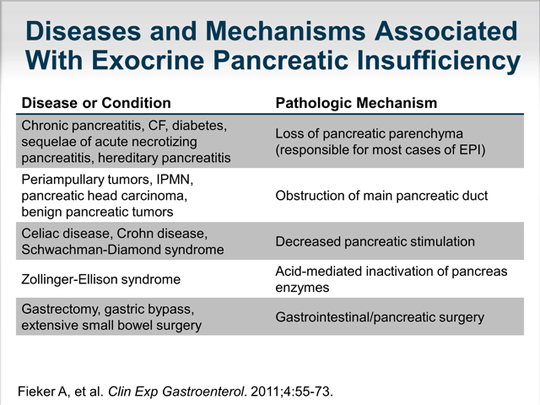

Below is a table of EPI diseases. AzurRx’s lead candidate, MS1819, is in clinical trials and may prove itself able to treat chronic pancreatitis and cystic fibrosis.

(Source: Medscape)

Drug Candidates

The company says that it plans to initiate Phase 2a clinical studies for its MS1819 candidate. Its Phase 1 studies have so far demonstrated its safety and efficacy support when compared to porcine pancreatic extracts, or PPEs.

If proven effective, MS1819 will be used to treat patients with chronic pancreatitis and cystic fibrosis.

AzurRx believes that MS1819’s treatment potential is superior to existing PPE-based treatments, because PPEs “suffer from poor stability, formulation problems, possible transmission of conventional and non-conventional infectious agents due to their animal origins, possible adverse events at high doses in patients with CF (cystic fibrosis) and limited effectiveness.”

Its AZX1101 candidate is still in preclinical stage and needs additional funding to prepare its safety and toxicology data required to file an IND (Investigational New Drug) application with the FDA.

The company believes that AZX1101 has the potential to help prevent infections resulting from bacterial strains that are resistant to current beta-lactam antibiotic treatments.

Competition

MS1819’s main competitors are existing PPEs, marketed by large pharmaceutical companies AbbVie (NYSE:ABBV), Johnson & Johnson (NYSE:JNJ) and Actavis/Allergan (NYSE:AGN).

The existing US market for PPEs in 2015 was in excess of $1 billion per IMS Health 2015 prescription data estimate. Furthermore, the market has been growing at a CAGR of 22% since 2009.

Regarding its AZX1101 candidate, the company says it is aware of only one other beta-lactamase candidate under development in the U.S. It believes that this other protein may have only limited efficacy for specific classes of antibiotics rather than a wide variety of antibiotics that it expects its compound to cover.

Financials

AzurRx Biopharma is offering 2.1 million shares in its IPO, approximately 20% of the company’s common stock at a proposed price of $7.00 per share, subject to customary over-allotment allocations to the underwriters.

The company says it plans to use 50% of the IPO proceeds to continue development of its lead candidate, MS1819, and 10% of the proceeds to advance its preclinical AZX1101 program. Another $356,000 will be used to repay convertible debt, leaving the remainder for general corporate purposes.

AzurRx had $2.1 million in cash as of March 31, 2016, and $2.3 million in current liabilities. It has had no revenues and an accumulated deficit of $10.3 million to-date.

According to its recent S-1/A filing, on June 15, 2016, the company’s CPA “expressed substantial doubt about (AzurRx’s) ability to continue as a going concern.

IPO Opinion

AzurRx is a tiny, clinical-stage biopharma that is scientifically backed by substantial European researchers.

It appears to have demonstrated that its lead candidate does not cause harm in humans, but is still a long way from demonstrating efficacy and an improved risk profile compared to existing PPE-based treatments.

It will likely need significantly more investment in the 15- to 18-month time frame in order to produce the next valuation increase, assuming its lead candidate continues to pass clinical trial milestones.

At this point in its development, it is too risky to recommend purchasing its initial offering shares. Wait for more clinical data on its lead candidate before considering this stock.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.