Betting The Farm With A Portion Of Your Portfolio – Part II

“Time is the coin of your life. It is the only coin you have, and only you can determine how it will be spent. Be careful lest you let other people spend it for you.”

Carl Sandburg

Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria”

Sir John Templeton

“Life and investing are long ballgames.”

Julian Robertson

Introduction

As someone who has “Bet The Farm”, and lost before (I have won before too), why on earth would I embark on my second, in a series of articles, that articulate the merits of this strategy?

The answer is simple. In a world of uniformity, the rewards for being different, for a portion of an investor’s portfolio, have never been greater.

The key, of course is position sizing, asset allocation, and overall portfolio strategy. Fortunately, for investors, we live in a world of low return expectations, given the current valuations of stocks and bonds.

Since traditional investment choices, meaning bonds and stocks, are offering future returns that are projected to be negative in real terms for the next decade, the risk of being different is not as great as it was in 2009, or 1990, or 1980.

In fact, today, the opportunity cost of not being in traditional stocks and bonds may actually be a benefit, if projections of future negative returns prove accurate. Think about that for a minute, the best thing to do for a large portion of your portfolio may be to sit in cash, do nothing, and wait for better prices.

Summing it up, if nearly everything is overvalued, would it not make sense to look for the undervalued assets, and concentrate in these undervalued sectors, while underweighting the overvalued sectors?

Thesis

A concentrated options focused portfolio, that comprises an appropriately sized position in an investor’s overall portfolio, could enhance overall returns, while adding acceptable levels of risk, given the prevailing return expectations.

A Low Return Environment Is Getting Lower

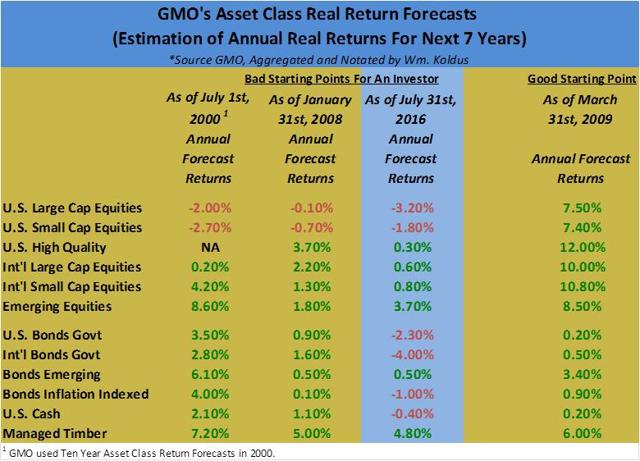

Throughout my writing on Unique Finance over the past seventeen months, I have consistently used a table that I have put together showing projected future “real returns” for asset classes, using data from Grantham, Mayo, Van Otterloo & Co., LLC, who are better known in the investment world as GMO.

GMO is widely regarded as a premier, value investment manager, and this is validated by the fact that they have over $100 billion in assets under management. Thus, they have won a significant number of sizeable clients via their long-term investment views and results.

Personally, I think they are the preeminent asset class forecaster. On that note, the following table shows their projected real returns, on an annual basis, as of July 31, 2016, for the next seven years.

Looking at the table above, the returns expectations should be sobering to most investors. In a world where pension plans routinely build gains of 8% for stocks and 4% for bonds into their long-term actuarial calculations, U.S. large-cap equities, are projected to have a negative real return of 3.2% annually.

Even more amazing, U.S. government bonds, a traditional safe-haven, are projected to lose 2.3% annually in real terms. Even cash, high on the food chain as a safe-have asset, is projected to have a modest negative real return, as inflation erodes the small amount of interest that is paid on these deposits.

The only asset class that looks attractive is managed timber, and the largest public proxy for this trade, Weyerhaeuser Co. (NYSE:WY), does not look particularly cheap, after a strong run-up from 2012, though it does sport a fairly robust dividend of nearly 4%, in a world where ten-year U.S. Treasuries yield closer to 1.5% currently.

On this note, roughly 60% of S&P 500 Index stocks have yields higher than the ten-year U.S Treasury, when it is typically closer to 10% historically on average. Where is the bubble centered?

The Merits Of A Valuation Methodology

Whether you agree with GMO’s asset class forecast projections or not, there is a benefit of forecasting future returns. This benefit is that it gives you a point of reference. This works form a macro view, or from an individual, bottom-up stock view.

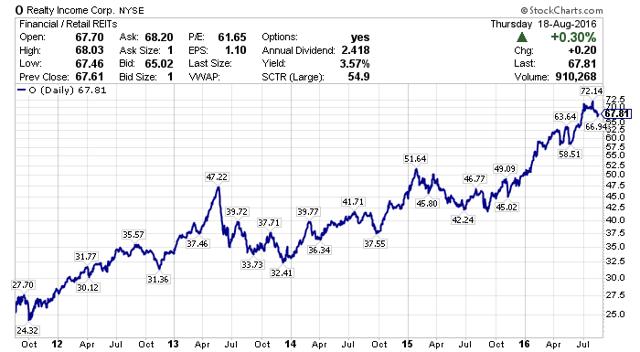

For example, I believe the current fair value of Realty Income is in the $40-$50 per share range. Thus, if I was buying this security, I would look to accumulate a position at or below fair value.

From the chart above, Realty Income shares have been above the high end of this $50 band for all of 2016. Thus, according to my logic, I would not be buying shares if I were a long-term investor. This reference point, which is often calculated using fundamental measures of value, gives you a compass in the wild, uncharted ocean that is the stock market.

The example with Realty Income is a bottom-up example of stock valuations. Top-down and macro investors are making the same calculations for the broader markets to determine the correct asset allocations, from their perspective, in order to deliver the highest potential risk adjusted returns.

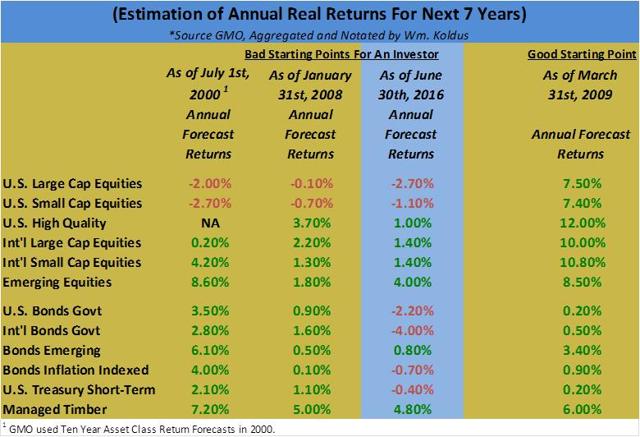

Circling back to GMO, whether you agree with their asset class forecasts or not, they stay true to their reference point. To illustrate this, look at their June 2016, asset class real returns forecast.

If you compare GMO’s July 31st, 2016 asset class return forecasts (the first table I showed), to June’s above, you will notice that all of the projected annual real returns are lower, and this makes sense, since both the stock and bond markets appreciated during the month of July, and this has been true for calendar 2016, and for the past five years. Almost everything in the U.S., with some notable exceptions that have been painful to me personally, has been going up the past five years.

This is shown by the performance chart of the SPDR S&P 500 Index ETF (NYSEARCA:SPY), the iShares Russell 2000 Index ETF (NYSEARCA:IWM), the SPDR S&P Dividend ETF (NYSEARCA:SDY), the Vanguard REIT ETF (NYSEARCA:VNQ), and the iShares 20+ Year Treasury Bond ETF (NYSEARCA:TLT).

In the U.S. market, this widespread appreciation has led to the current historically high valuations present today, with dividend growth stocks leading the way over this time frame.

Where Are The Values, What Has Not Appreciated?

Even with their tremendous reversal and rally in 2016, commodities, commodity stocks, and emerging markets have underperformed their developed market peers, particularly the U.S., by a material amount over the past five years.

The five-year performance graph of the SPDR S&P Metals & Mining ETF (NYSEARCA:XME), the VanEck Vectors Gold Miners ETF (NYSEARCA:GDX), the Energy Select Sector SPDR Fund ETF (NYSEARCA:XLE), and the iShares MSCI Emerging Markets ETF (NYSEARCA:EEM), relative to the S&P 500 index, shows a startling contrast in results.

Believe it or not, based on the above, all of these out-of-favor sectors are having a terrific 2016, as the reversion-to-the-mean trade kicks in.

Gold stocks, as measured by the GDX, are up 124% year-to-date in 2016, and the steel heavy XME is up 88%. Even the energy markets have shown impressive returns, as both crude oil (NYSEARCA:USO), and natural gas (NYSEARCA:UNG) have bounced back.

The XLE is up 19%, as large-cap energy companies like Exxon Mobil (NYSE:XOM), up 17% YTD, Chevron (NYSE:CVX), up 19% YTD, have trended higher, but the impressive price action is in formerly out-of-favor names like Chesapeake Energy (NYSE:CHK), now up 38% YTD, Kinder Morgan, up an impressive 56% YTD, and Williams Companies, up 17%, recovering from a more than a 50% loss earlier in the year.

Betting The Farm On Out-Of-Favor Assets

When most asset classes are showing negative projected returns for the next decade, it makes sense as an investor to look for the undervalued, out-of-favor companies.

Throughout 2016, I have attempted to identify these bargain-bin priced companies with a series of public Unique Finance articles, which I have headlined with the “Too Cheap To Ignore” moniker.

Additionally, I have founded “The Contrarian”, a premium research service on December 7th, 2015. At the heart of The Contrarian are four model portfolios, including the “Bet The Farm” Portfolio, an options focused portfolio, the “Best Ideas” Portfolio, a concentrated equity portfolio, the “90/10” Portfolio, a 90% cash portfolio that I believe will outperform a traditional 60% stock/40% bond portfolio over the next decade, and a long/short portfolio, that I call the “Contrarian All Weather” Portfolio. In 2016, through August 15th, these portfolios were up 312.2%, 58.0%, 7.0%, and 19.2% respectively, compared to the S&P 500 Index’s gain of 8.3%.

How did these portfolios achieve their impressive absolute and relative performance? The answer is simple, they were overweight undervalued, and out-of-favor stocks.

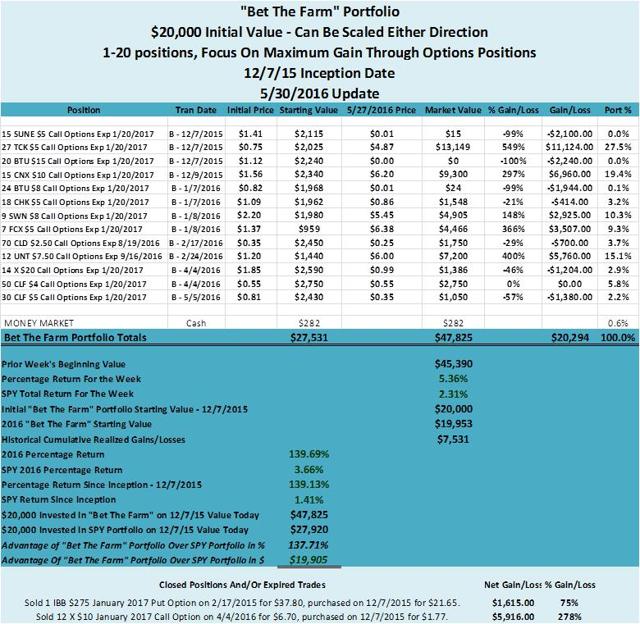

To provide you a preview of the “Bet The Farm” Portfolio, I have copied and pasted the portfolio snapshot that I sent to subscribers on 5/30/2016.

While returns were impressive at the time, up 139.7% through May 27th, 2016, the returns have obviously improved further, to get to the 312.2% return accrued through August, 15th, 2016.

From examining the positions in the portfolio, you will notice that nearly all of the portfolio positions were held in strongly out-of-favor stocks, at the time they were purchased. Now, with the benefit of hindsight, certainly some of these positions did not work out, including Peabody Energy (OTCPK:BTUUQ), and SunEdision (OTCPK:SUNEQ).

However, holding a basket of these undervalued stocks has led to big gains, with their options doing even better, as Teck Resources (NYSE:TCK), CONSOL Energy (NYSE:CNX), Chesapeake Energy, Southwestern Energy (NYSE:SWN), Freeport-McMoRan (NYSE:FCX), Cloud Peak Energy (NYSE:CLD), Unit Corporation (NYSE:UNT), U.S. Steel (NYSE:X), and Cliffs Natural Resources (NYSE:CLF) have all bounced back strongly in 2016.

If options are not your cup of tea, I understand that, and I can sympathize, but the same core principle applies, in that having a portion of an investor’s portfolio, say 10%, which is an arbitrary number and this percentage ultimately needs to be decided on by an investor, allocated to an undervalued, out-of-favor basket of securities, provides a differentiated potential avenue of performance, in a world where investment returns seem to be increasingly correlated.

Portfolio Strategy & Asset Allocation 2011-2016

Portfolio construction is a combination of art and science. During my career, I have worked in institutional investment environments, where the efficient market theory was promoted, mostly by those with an academic background, and the heavy lifting of alpha generation was left to the alternative investments, specifically direct hedge fund strategies, private equity, and private real estate. Investors can think of this asset allocation strategy as the endowment model, popularized by David Swensen’s popular book, “Pioneering Portfolio Management: An Uncoventional Approach To Institutional Investment”.

While there is some merit to this view over the long run, in my opinion, I believe that even the “beta” markets are inherently inefficient, particularly over the shorter-term and intermediate-term timeframes, due to human behavior and emotions that impact market prices.

Building on this, the influx of assets into passive investments, like the Vanguard Total Stock Market ETF (NYSEARCA:VTI), which when combined with its siblings on the mutual fund side, the Vanguard Total Stock Market Index Funds (MUTF:VTSMX), (MUTF:VITSX), now constitutes the largest index strategy in the world, has distorted prices, as index money continues to bid up the largest market capitalization companies, with no discretion for their valuations. Adding fuel to the fire, there is no sign of a slowdown into these passive stock market benchmarks, as many active managers have had a black eye over the past five years.

Why have the past five years been so detrimental for active managers? The answer can be found in the fact that beginning in 2011, specifically in April of 2011, the performance of reflationary assets, which have been historically tied to global growth, including commodities, commodity stocks, and emerging market equities, along with financial stocks and cyclical companies, diverged dramatically from the broader U.S. stock market.

Thus, 2011 marked the start of an era where the largest U.S. companies became safe-haven, deflationary assets in a low global growth world. This transformation was so remarkable, and so out-of-step with the historical role of equities, that I wrote an article for Unique Finance on November 23rd, 2015 discussing how U.S. stocks had improbably become a deflationary asset.

Institutional and retail money flow has exacerbated the self-reinforcing cycle, where the largest market capitalization companies in the world, which are mainly domiciled in the U.S., became the ultimate recipient of investment dollars. This created a distortion in investment valuations between the favored destinations for fund flows, like the United States, and the shunned destinations like China. However, calendar year 2016 has seen a reversal of this five-year trend, as out-of-favor asset classes are now outperforming to a remarkable degree.

In similar fashion, value stocks are having a renaissance year in 2016, after underperforming their growth counterparts over the 2011-2015 time frame. The combination of the revival of out-of-favor cyclical growth plays, along with the reversion-to-the-mean trade in value versus growth, has revitalized the active investment management industry, as historically, many of the outperforming active managers have favored value strategies.

The YTD performance of the iShares Russell 1000 Value ETF (NYSEARCA:IWD) compared to the iShares Russell 1000 Growth ETF (NYSEARCA:IWF), shown in the first chart below, shows the positive outperformance by large cap value stocks in 2016 (10.1% versus 6.5%). The second chart, shows the performance of the iShares Russell 2000 Value ETF (NYSEARCA:IWN) versus the iShares Russell 2000 Growth ETF (NYSEARCA:IWO), and there, the gap is even more dramatic, with IWN outpacing IWO 14.2% to 6.1% in 2016.

Portfolio Construction & Risk

If simply buying value stocks, which are out-of-favor by nature, has proven to be the best performing investment strategy over time, and it has according to Ibbotson data, Warren Buffett in his now famous May 17th, 1984 white paper, The Superinvestors of Graham-and-Doddsville, and nearly all anecdotal evidence, including the birth of the now prevalent fundamental value indexing strategy, why doesn’t everyone do it? And, taking this concept a step further, why doesn’t everyone invest in long-term options in out-of-favor, deep value stocks?

The answer, of course, is that it is not that simple. Typically, in the investment markets, when a higher degree of return is anticipated, a higher degree of risk accompanies these enhanced return opportunities, and deep value investing, particularly with options, carries its own set of unique risks, including the potential of a total loss of investment, as options could, and do, expire worthless, if the underlying security does not revalue in your designated time parameter.

The positive aspects of using options to implement a portfolio of deep value securities is that they define risk, leverage upside, providing the often discussed, but rarely achieved asymmetrical risk profile. Further, option investing provides a definitive time window for your thesis to play out. Finally, an options portfolio can be a relatively small percentage of your total portfolio, but have a positive outsized impact if market developments play out according to the investors range of probabilities and expectations.

Practitioners of deep value investing, and using options to invest in out-of-favor equities, both specialized types of investment analysis and implementation, including your humble author, usually have the scars to show from their years of learning experiences.

That is why it is imperative for each investor to consider their overall portfolio allocations, and know what to expect from their specific portfolio strategies.

In the current environment, where stocks and bonds offer negative real returns, over the next decade in my opinion, it is an ideal time to consider alternative investment strategies. That is the premise behind a series of articles highlighting why I expected a 90% cash portfolio to outperform a traditional stock and bond portfolio over the next decade.

If you have made it to this point, as a reader, you have logically connected the dots to the next step, which would be, instead of allocating 10%, or whatever number you determine in your own risk budget, to a basket of deeply out-of-favor equities, the asymmetrical return profile, and impact on the portfolio, would be amplified using an options strategy for the aforementioned risk bucket.

Out-Of-Favor Versus In-Favor Investments

Since asset allocation is one of the primary driver of overall portfolio returns, and nearly all asset classes are overvalued today, and are projected to deliver negative real returns over the next decade, what is an investor or portfolio manager to do?

The answer, again, is simple, in my eyes, and that is to look for undervalued securities in the out-of-favor asset classes, and then make targeted bets to benefit from the reversion-to-the-mean trade to rectify this undervaluation.

From my perspective, the tremendous underperformance of commodities, commodity stocks, and emerging market equities from 2011-2015, in a previously described deflationary world, has created a dream environment of historically cheap securities, and this remains the sweet spot of the current opportunity set, in my opinion.

Building on the narrative of reflation, and a rotation out of the safe-haven of the U.S., financial stocks, another beaten up and bruised sector, stand to benefit, in my opinion, and there is a particular area within financials that is appealing to me right now.

More broadly, investors should consider the relative valuations of the securities they own, comparing the valuations of Apple (NASDAQ:AAPL) to Facebook (NASDAQ:FB) for example, as I have done, coming to the conclusion that the former is undervalued, and the latter is incredibly expensive at today’s prices.

Another way to look at relative valuations is to compare a category leader like Amazon (NASDAQ:AMZN), which seems extremely expensive, and behaviorally in-favor, and over-owned by investors, from my perspective, to a more specialized niche play, that is out-of-favor, like Restoration Hardware (NYSE:RH), which I highlighted in a July 28th, 2016 brainstorming article to my subscribers.

The Takeaway – Consider An Alternative Strategy

With stock and bond valuations both residing at historic highs, now is a good time for investors to revisit their portfolio allocations, investment strategies, and individual stock positions.

A review might yield some surprising conclusions, including a preponderance of overvalued securities, and a relative lack of the underperforming, value-oriented investments.

Investors, speculators, and traders should remedy this condition, by considering alternative, non-correlated investments and investment strategies.

In summary, I firmly believe that a long/short investment strategy should represent the core of an investor’s portfolio today, and for the foreseeable future, until future return expectations are considerably higher for both stocks and bonds.

Building on this narrative, until an environment of better prospective returns exists; I believe that investors should consider a barbell approach, holding a higher percentage of their portfolio in cash, while making more concentrated bets, with a smaller percentage of their portfolio, to target outsized returns.

In closing, to receive my future public articles please click the “Follow” button above. If you are interested in joining a unique, growing community of contrarian, value-oriented investors, and would like to see all of the historical trades and current positioning of the “Bet The Farm”, and the “Best Ideas” Portfolios, please consider signing up for my premium research service, “The Contrarian“, on Unique Finance. This service has been highly rated by subscribers, and those of you interested should check out the reviews. Thank you for your readership.

Disclosure: I am/we are long THE POSITIONS IN “THE CONTRARIAN” PORTFOLIOS.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.