Equus Total Return Fund: A 2-For-1 Opportunity For Value Investors

Equus Total Return Fund’s 2nd Quarter NAV Increase

The Equus Total Return Fund, Inc (NYSE:EQS) recently released its 2nd quarter net asset value. NAV increased by roughly $2 million or just over 5% to $3.13. This is the first significant increase in NAV for the fund in over a year and likely not the last. Portfolio value had been bumping along near historic lows for many quarters, suffering from what has been termed a general malaise in the BDC market and unfortunate timing with the majority of the fund’s energy investments. Now it looks like the loss leaders have stabilized enough to let other segments of the portfolio shine.

Gains in portfolio value were made in two areas, the 18.7% stake in Pallet One and the equity stake in BDC MVC Capital (NYSE:MVC). The stake in MVC gained nearly 10% during the quarter, primarily to a resurgence of interest in high yield BDC’s, with shares rising to $8.04 from $7.33. In addition to capital appreciation Equus also received an additional 7,973 shares of MVC as a dividend which led to a net increase of $0.3 million to the portfolio. This portion of the EQS portfolio is now worth about $3.6 million, down 38% from purchase.

The biggest gains were made by Pallet One which remains the top investment in the portfolio. This company has seen significant gains in its trailing 12 month revenue and profits over the past 4 quarters that have led to substantial revaluation. This quarter alone saw fair value increase by 23% or $2.7 million to $14.3 million, the original cost of this investment was only $350,000. Equus now holds more than 18% of the company which is one of the largest manufacturers of shipping pallets in the US.

Combined gains from these two investments were offset by losses in the energy sector. Equus Energy, a wholly owned subsidiary incorporated for the purpose of investing in the oil and gas arena, posted an 11% decline in value losing $0.5 million over the course of the quarter. The losses are due to the closing of 18 unproductive wells and the impact of lower forward oil and gas prices on expected earnings. In total, Equus Energy owns more than 110 operating and non-operating wells spread across 13 properties in Texas and Oklahoma as well as a stake in the Eagle Ford Shale play. These investments were purchased for more than $7 million, just before the bottom fell out of the energy market. Value of the energy portfolio now stands closer to $4 million.

There are a few other holdings within the portfolio but they represent only a small portion. The Equus Media Development Company is worth only about $200,000 and not expected to produce much, no pun intended. This is one of the original investments, worth less than 20% of its original value. Two newer investments, worth about $3 million, may have better results. Both are in the form of debt investments and both are yet to be collected on.

Where’s The Value?

The portfolio isn’t pretty. A combination of unfortunate investing strategy, capital destroying dividend payments, plunging oil prices and the aforementioned malaise in BDC investing helped to drive EQS shares to historical lows and they have not recovered. There is some value left in the portfolio but the real value is in cash holdings, about 60% of assets (not including liabilities), the investments are just icing on the cake.

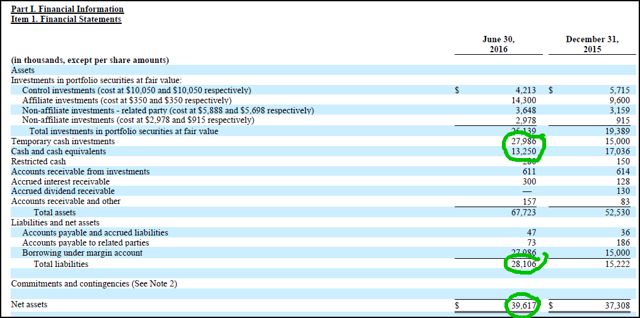

- Cash and temporary cash investments total more than $41 million, which, accounting for liabilities, is $1.04 of NAV ($13.25 million in cash less liabilities/12.67 million shares outstanding). This means 50% of the investment portion of the portfolio could be written off and there would be enough cash to provide a premium value to today’s share prices.

- Third party valuations put the portfolio holdings at over $25 million which equates to about $1.97 of NAV, slightly higher than today’s share value.

- There are some liabilities to consider. Taking them into account leaves the fund trading at a near 50% discount to NAV with free cash equaling 34.45% of NAV.

- With shares trading at a 45% discount to NAV (accounts for liabilities) what value investors get is a two-fer. You pay one low price, about $1.70 as I am writing this, and get an investment portfolio and cash holdings with combined worth nearly double the share price.

source EQS 10Q

If all things remain the same this fund could easily see a significant increase in share price as investors begin to capitalize on the discount. Assuming NAV holds stable, merely narrowing to a point that cuts the discount to 25% would add about $0.80 or 30% to today’s share prices.

Looking forward there is the possibility of a merger/acquisition with MVC Capital but there has been little news of that. The merger is important as EQS status as a BDC depends on it, remember the original stake in MVC was part of a share exchange which initiated a reorganization of the fund. This deal began several years ago and has yet to be finalized. Two possible outcomes are present; EQS will merge/consolidate into MVC, or EQS will terminate its classification as a BDC and restructure as a publicly traded company.

If the merger does move forward share holders will benefit from the larger BDC, better management and the proper deployment of cash. If not, a liquidation or restructuring of the fund could provide total returns in excess of 100%. Even without liquidation there is plenty of cash that could be returned to shareholders. Regardless the outcome, EQS is a deeply undervalued fund ripe for value investors.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in EQS over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.