First NBC Bank Holding: Underfollowed And Unloved, But Not Without A Reason

The bank

Through its wholly-owned subsidiary – First NBC Bank, a Louisiana state non-member bank – First NBC Bank Holding Company (NASDAQ:FNBC) provides a wide range of financial services in New Orleans (metropolitan area), Florida (panhandle) and Mississippi Gulf Coast. As of December 31, 2015, the company had 39 banking offices.

Real estate

With the main income source being customer loan issuance, First NBC is strongly dependent on Louisiana State’s real estate prices. As of December 2014, approximately 50.4% of total outstanding loans issued were consumer and commercial real estate loans (I know it is 2016 already, but please bear with me). A major part of the company’s business is concentrated in the New Orleans metropolitan area:

We are more sensitive than our more geographically diversified competitors to adverse changes in the local economy.

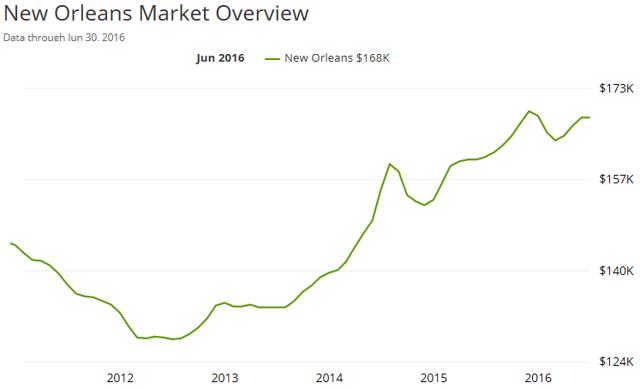

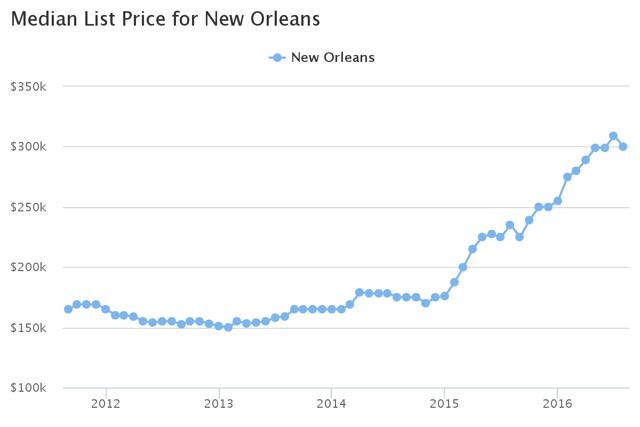

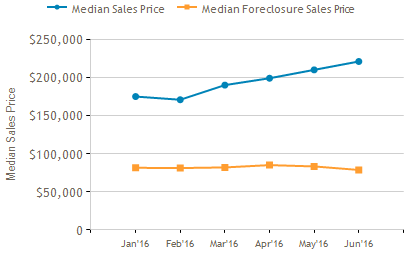

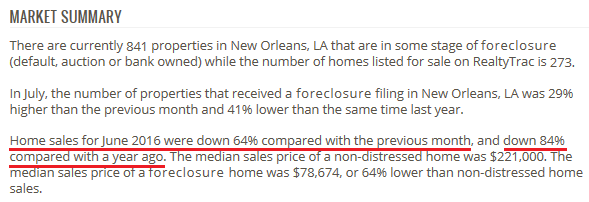

The New Orleans real estate market has been on the rise since 2012-2013 and it can be argued that the top has already been reached. Below is the market data provided by Zillow, Movoto and RealtyTrac.

Source: Zillow.com (2016).

Source: Movoto.com (2016).

Source: Realtytrac.com (2016).

Source: Realtytrac.com (2016).

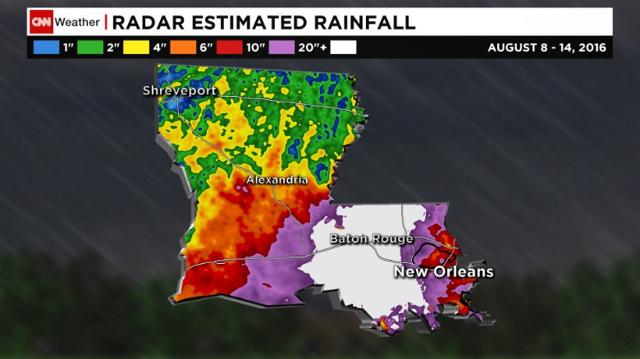

Louisiana flood

Finally, most of the readers might be aware of the recent disaster happening in Louisiana. As a result of 6,900,000,000,000 gallons of rain in one week’s time, total number of damaged houses is estimated at 40,000, according to CNN. Even though the company has not commented upon the situation yet, it is almost certain that the large-scale flood, being a once-in-500-years phenomenon, might have a substantial impact on the company’s financials.

Source: CNN (2016).

Tax credit investments

One of the differentiating factors of the company’s business model is the tax credit investments. Here is a quote from the company’s President and CEO Ashton J. Ryan, Jr. (emphasis mine):

The most discussed and misunderstood part of our business is our investment in tax credits. Over the years, we have greatly expanded our financial statement disclosure in order to provide transparency on this aspect of our business. […] I am often asked why we invest in tax credits when most other banks our size do not. My response to that query follows: our investment in tax credits is an integral part of our commercial real estate business. We are commercial lenders with an emphasis on commercial real estate, and we use tax credits to enhance our commercial real estate lending. Our investment substantially increases the equity in real estate development projects which qualify for tax credits and thus results in lower loan to value and higher debt service coverage ratio, both major risk mitigators for our lending risk profile. Also, our understanding of tax credits and our investment in the projects, makes us the lender of choice for real estate projects in our markets, which has enabled us to dominate this type of lending in New Orleans since tax credit equity also enhances owner/developer profits.

Other reasons mentioned include community development and shareholder value maximization intentions.

Since tax credits are having a positive impact on the company’s tax bill, the strategy is certainly paying off. However, there is no free lunch. As a consequence, First NBC is often exposed to riskier assets as federal tax credits are only being offered for selected projects. Furthermore, the bank notes that collateral tied to these types of loans is often illiquid and thus significantly raises the possibility of loan loss provision increases in the future.

As a side note, it is important to mention that the company views its tax credit investments as a crucial strategy component:

[m]anagement believes that understanding the impact of the Company’s investment in tax credit entities is critical to understanding its financial performance on a standalone basis and in relation to its peers.

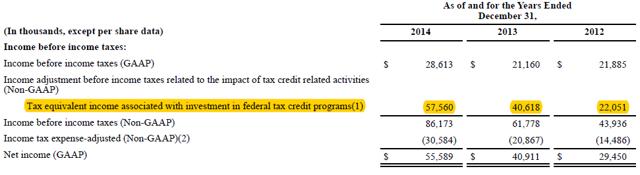

The sole tax credit impact on the company’s bottom line is expressed in a tax expense decrease, which is undeniably good. There might be some future profitability concerns, however.

If expressed as a non-GAAP income measure, the tax credit investment impact accounts for a substantial part of the bank’s bottom line.

Source: First NBC’s 2014 annual report (2015).

The tax credit-motivated projects First NBC invests in (as of December 2014) are mainly divided into 3 categories:

- Low-Income Housing – tax credits over a period of either 10 or 15 years.

- Federal Historic Rehabilitation – tax credits in the year of the occupancy certificate issuance.

- Federal New Markets – specific terms.

The tax credit investment only further intensifies the bank’s real estate exposure.

From the company’s 2014 annual report (emphasis mine):

For Low-Income Housing and Federal Historic Rehabilitation Tax Credits, the Company invests in a tax credit entity, usually a limited liability company, which owns or master leases the real estate. The Company receives a 99.99% for Low-Income Housing and a 99% for Federal Historic Rehabilitation nonvoting interest in the entity that must be retained during the compliance period for the credits (15 years for Low-Income Housing credits and five years for Federal Historic Rehabilitation credits). In most cases, the interest in the entity is reduced from a 99.99% and 99% interest to a 5% to 25% interest at the end of the compliance period. Control of the tax credit entity rests in the 0.01% and 1% interest general partner, who has the power and authority to make decisions that impact economic performance of the project and is required to oversee and manage the project. Due to the lack of any voting, economic or managerial control, and due to the contractual reduction in the investment, the Company accounts for its investments by amortizing the investment over the estimated holding or contract period. Any potential residual value in the real estate at the end of the compliance period will be recognized upon disposition of the investment.

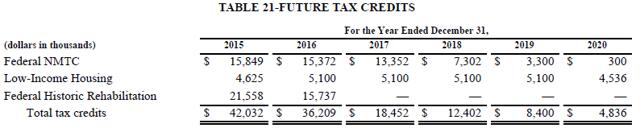

As of December 2014, the expected future tax credit amounts on existing investments were as follows:

Source: First NBC’s 2014 annual report (2015).

In order to continue growing the tax credit benefits, the company has to invest more and thus even further increase its real estate exposure.

Operating performance

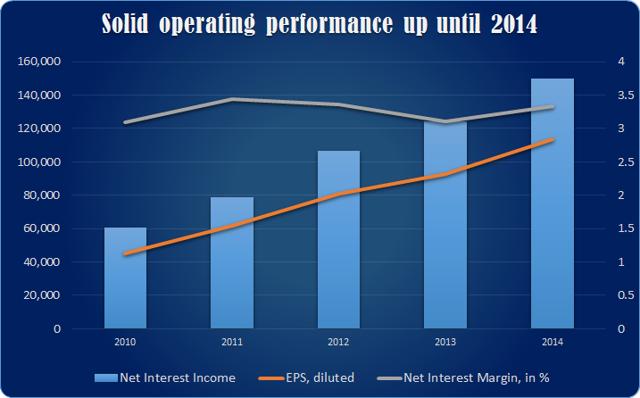

Despite the near-term headwinds, past operating performance has been reasonably strong.

Net interest income (in $1000s), diluted EPS and net interest margin of First NBC, 2010-2014. Source: 2014 annual report.

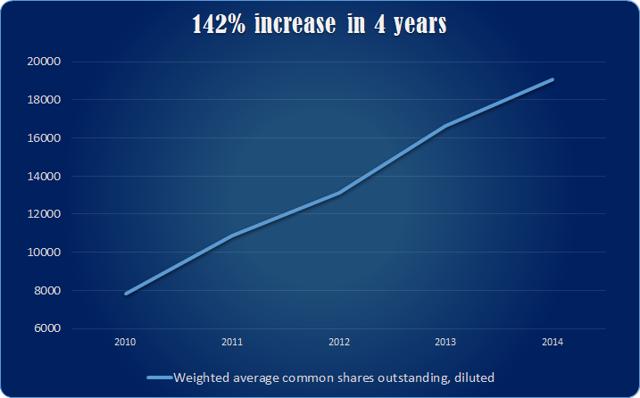

On a less positive note, significant share dilution has been taking place.

Weighted average number of common shares outstanding, diluted (in 1000s) of First NBC, 2010-2014. Source: 2014 annual report.

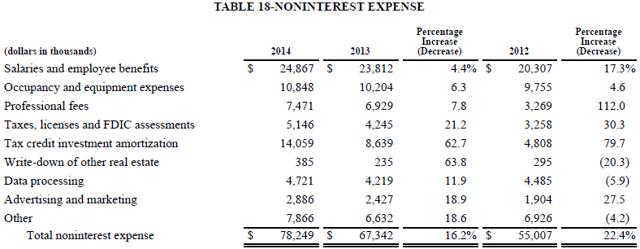

Meanwhile, all of the non-operating expenses have been on a rise lately.

Source: 2014 annual report.

Rising competition and busted growth?

The current low-rate environment might continue to fuel increased competition in the banking sector. Here is a quote from the latest annual report (emphasis mine):

Many of our competitors are larger and have significantly more resources, greater name recognition, and more extensive and established branch networks than we do. Because of their scale, many of these competitors can be more aggressive than we can on loan and deposit pricing. Also, many of our non-bank competitors have fewer regulatory constraints and may have lower cost structures. We expect competition to continue to intensify due to financial institution consolidation; legislative, regulatory and technological changes; and the emergence of alternative banking sources. Increased competition could require us to increase the rates that we pay on deposits or lower the rates that we offer on loans, which could reduce our profitability.

At the same time, the bank acknowledges the fact that the recent acquisition-fueled growth might not continue in the future:

Our growth has been aided by acquisitions of our local competitors, which may not continue […] We may not be able to manage the risks associated with our anticipated growth and expansion through de novo branching, which could adversely affect our profitability.

Reporting issues

In April 2016, the company announced that the statements for 2011 to 2014 cannot be considered reliable due to material accounting errors in the 2015 annual report (which has not been published yet), The Advocate wrote in April. The mistakes were related to the federal and state historic rehabilitation tax credit entities.

Due to the delay, the company has received a non-compliance notification from Nasdaq earlier that month. From the announcement:

Under Nasdaq rules, First NBC has 60 calendar days from the date of the letter, or until June 3, 2016, to submit a plan to regain compliance. If its plan is accepted, First NBC may be eligible for a listing exception of up to 180 calendar days or until September 26, 2016 to regain compliance.

In June, the company’s plan has been successfully submitted and accepted by Nasdaq.

First NBC has officially published a delay-related PR-announcement on August 15, 2016. The announcement included a paragraph regarding the 10-Q (quarterly report) for the period ended June 30, 2016. Even though the company had previously agreed to publish the past due filings before September 26, 2016, the fact that it has not published the Q1 2016 report makes it non-compliant once again (Nasdaq Listing Rule 5250(c)(1)).

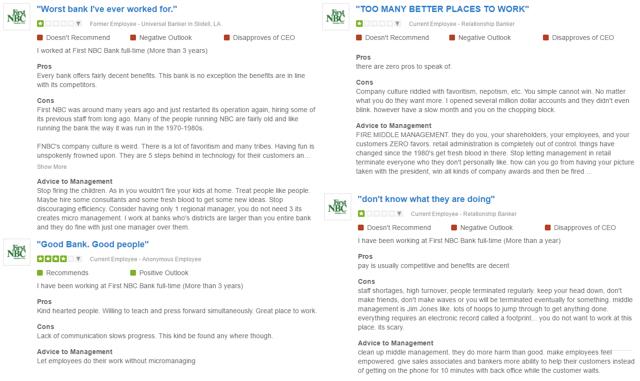

Concerning reviews

The company is no stranger to criticism. Even though employer and bank service reviews are often positive, of note is the fact that the bank is often viewed as old-fashioned when it comes to service availability and technology. Certain employees are also criticizing the bank for excessive micromanagement and inefficiency.

Here are some of the Glassdoor reviews. The webpage might be of interest to those interested in the stock.

Source: Glassdoor (2016).

Other concerning reviews might be found on Yelp and the comment section of neworleanscitybusiness.com.

Conclusion: underfollowed and unloved, but not without a reason

So, what do we have here? Let’s make a list.

- Intense competition;

- Diminishing growth opportunities;

- Real estate exposure risk (taking into account the Louisiana flood);

- Financial reporting difficulties;

- Mixed customer and employer reviews;

- Significant share dilution;

- Weak sentiment and a downtrending stock.

Source: StockCharts.com

Source: GuruFocus (2016).

Even though the stock is not heading towards zero, it is important to note that the ongoing reporting issues and the Louisiana flood’s impact might continue weighing on the stock’s performance over the medium term. Despite the stock’s performance, short interest has been trending lower and might rebound in the nearest future. Given the institutional ownership of 83.31%, the stock might experience substantial downside should the larger investors start unloading. It is difficult to come up with any developments that could have reversed the stock’s trend at this point. Even though the company might continue to demonstrate growth and solid operating performance in the future, the present headwinds are too significant. Meanwhile, the reporting issues and future lawsuit settlements create too much uncertainty going forward.

I assign FNBC a “Sell” rating.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This is not an investment advice. I am not an investment advisor.