Four Corners Is Becoming More Round But The Price Is Not Sound

We recently added Game and Leisure Property Trust (NASDAQ:GLPI) to our Intelligent REIT Lab. Although we are not in love with the company’s outsized exposure to Penn Gaming, we consider the REIT to be a Net Lease landlord and we wanted to broaden our research in the growing gaming sub-sector. (See recent GLPI article HERE).

Likewise, we also recently added Four Corners Property Trust (NYSE:FCPT) to our research lab back in May (see article HERE). While we were glad to see another Net Lease REIT on the menu, we weren’t ready to place an order because of the company’s “earnings stream that is highly dependent on consumer demand”.

Specifically, we are not fans of the FCPT because of the company’s “lack of diversification” and high reliance on Olive Garden to fund and grow its dividend.

Keep in mind, even when I go to a restaurant that has bad food or poor service, I will usually try it once again. It takes really bad service for me to never come back, yet I also believe in the three strikes you’re out rule.

So now with FCPT’s second quarter earnings in the history books I thought it would be a good time to check out the menu again. If we are going to sacrifice diversification (own a REIT with high tenant concentration) we believe that it’s prudent to pay close attention to the fundamentals including the risk-adjusted returns we are seeking.

What’s on the Menu?

In an article last December, I explained that “a Congressional tax bill proposed a ban on certain tax-free REIT spin-offs” that put the brakes on REIT spin-offs. This new bill now forces companies that want to spin-off their real estate into a REIT to be taxed – the distribution of either the real estate or operating assets would no longer be tax-free.

In other words, Darden Restaurants (NYSE:DRI) and FCPT were barely able to take advantage of the spin, just as the window was closing.

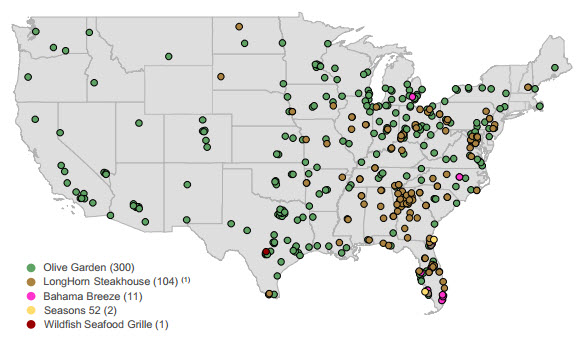

As you can see below, the FCPT portfolio now includes 424 properties in 44 states. The tenant/operators include Olive Garden, LongHorn Steakhouse, Bahama Breeze, Seasons 52, and Wildfish Seafood (as of Q2-16):

More recently (July 2016) FCPT said that it had acquired six Pizza Hut restaurants in the Chicago Naperville-Elgin MSA in Illinois and Indiana for $5.7 million via a sale and leaseback transaction. The company funded the acquisition with cash on hand.

The restaurants are 100% occupied under triple-net leases with terms of 20.0 years and an average going-in cash cap rate of 7.2%, exclusive of transaction costs. The operator owns over 150 units across multiple brands, and is one of the ten largest Burger King franchisees in the U.S.

Also, in August FCP announced the acquisition of a Wendy’s restaurant in Odessa, TX for $2.1 million. The company funded the acquisition with cash on hand. The restaurant is occupied under a triple-net lease with approximately 10 years of remaining term, and the transaction closed at a going-in cash cap rate of 6.5%, exclusive of transaction costs.

These latest transactions validate the fact that FCPT is beginning to diversify outside of its Darden-based portfolio and expand into other fast food categories.

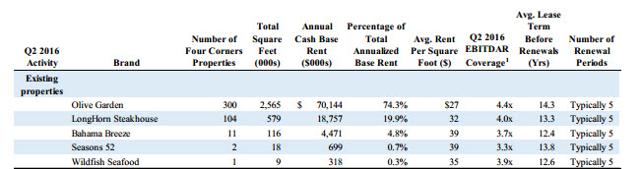

However, in the latest quarter FCPT’s cash rental income (without rent leveling on the existing rental portfolio of 418 properties leased to Darden) was $23.7 million for the quarter. These rents will increase annually by 1.5% for all 418 properties each November (in 60 days). Here’s a snapshot of the portfolio broken down by brands:

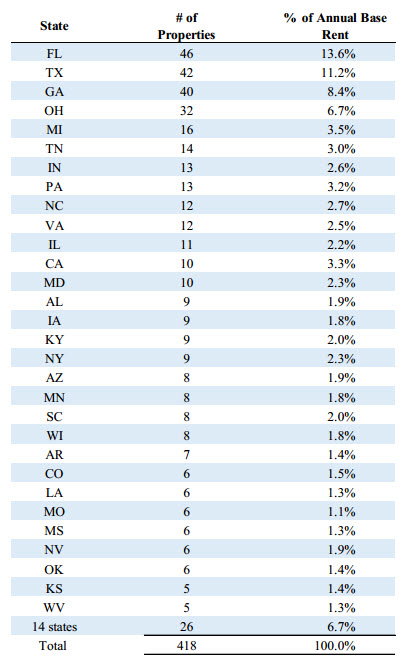

Although FCPT lacks revenue diversification the company does enjoy a well-balanced geographic model, with the largest concentration in Florida (13.6%), Texas (11.2%), and Georgia (8.4%).

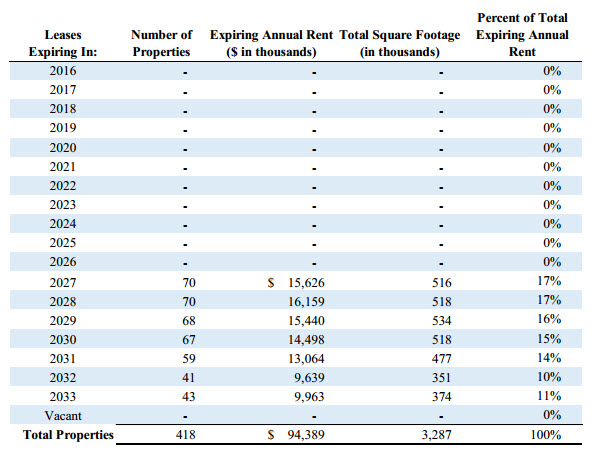

Also, FCPT has limited lease rollover risk as evidenced by the snapshot below: There are no lease maturities until 2027, and the weighted average lease term for the portfolio is just under 15 years.

The Balance Sheet

FCPT’s existing portfolio performed as planned during the second quarter notably DRI was upgraded by all three rating agencies recently and is now rated BBB flat, BBB flat and Ba3.

FCPT is comprised of high-quality restaurant properties that demonstrate strong operating performance. The REIT’s coverage ratios remain strong with cash interest coverage of 6x and net debt to cash EBITDA of 4.9x.

FCPT’s current low leverage will increase as the company begins to draw on its 4-year $350 million revolver to initially finance acquisitions.

Like most Net Lease REITs, FCPT is able to harvest organic cash flow growth from its portfolio of Triple Net leases. These individual leases allow for maximum flexibility in resetting rent levels and laddering expiration dates. The DRI leases (with FCPT) have built-in 1.5% rent escalators and fair market value adjustments that provide organic growth.

Most importantly, FCPT’s portfolio (tenants) is currently 100% investment-grade rated. While there’s an argument that one should not have all of their eggs in one basket, the one big egg in the FCPT basket is as solid as a rock.

The Latest Results

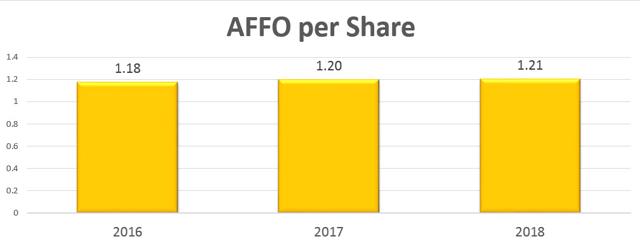

In the second quarter FCPT generated FFO of $.33 per share and AFFO of $.30 per share. The company does not provide guidance on acquisition levels or FFO and AFFO for the year but it did reconfirm its belief that the current portfolio will produce approximately $1.18 in AFFO per share. We have modeled AFFO through 2018 below:

Source: S&P Global Market Intelligence

Keep in mind that FCPT does not enjoy the same financial flexibility as the larger peers, Realty Income (NYSE:O) or National Retail (NYSE:NNN). In addition, FCPT competes with STORE Capital (NYSE:STOR), Spirit Realty (NYSE:SRC), and Agree Realty (NYSE:ADC) for investments.

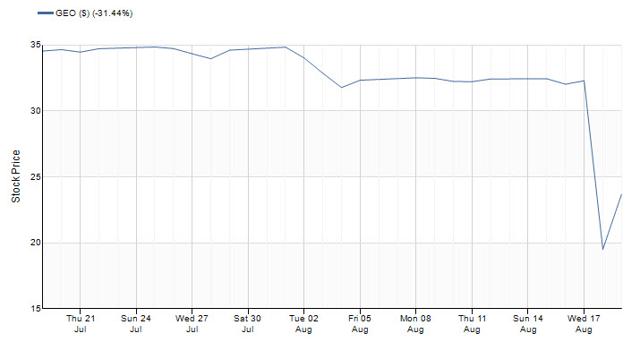

My point here is that FCPT must grow its business model and in doing so it must compete with more powerful forms of differentiation. While I like the concept of owning a REIT with high-quality sources of income, there is risk to putting all of the eggs in one basket. Case in point, look what happened to GEO Group (NYSE:GEO) last week when the DOJ said it was reducing and ultimately ceasing the use of private prisons.

For the near-term the risk for GEO is moderate but federal agencies pursue similar plans that ultimately could cause GEO’s business model to erode.

Source: S&P Global Market Intelligence

What does GEO have to do with FCPT? Take a look at this chart:

As you can see, Chipotle Mexican (NYSE:CMG) is still struggling from an E. coli outbreak that resulted in many patrons at its restaurants becoming ill and sales declining. The stock has yet to recover, is down almost 50% over the last year. Assume that there was a Chipotle REIT and you can get the picture.

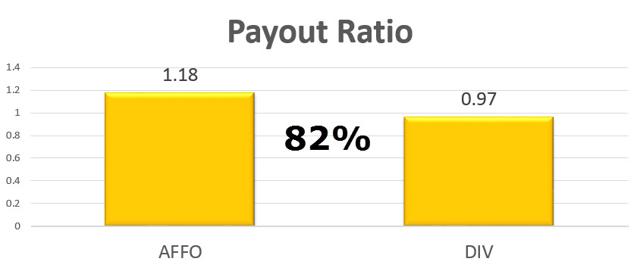

But, Chipotle is not Darden and currently the restaurant chain generates steady dividends for FCPT investors. The company’s annual dividend payout is $.97 per share and using the AFFO run rate of $1.18 per share the (dividend) income appears to be well-covered.

Source: S&P Global Market Intelligence

Sizing Up The Investment

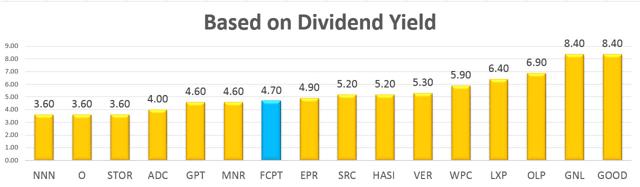

Let’s now size up the FCPT investment, first taking a look at dividend yield:

Source: S&P Global Market Intelligence

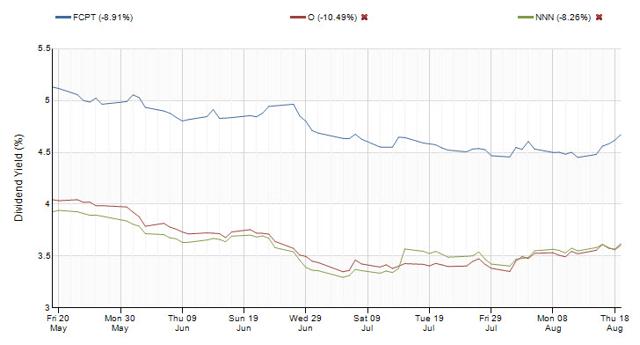

Based solely on “income” FCP appears to be attractive. The company’s yield today is 4.7% and that’s not too bad considering the “starve for yield” environment we are living in. Here is a better way to compare the risk premium being offered for FCPT compared with the stalwarts’ O and NNN.

Source: S&P Global Market Intelligence

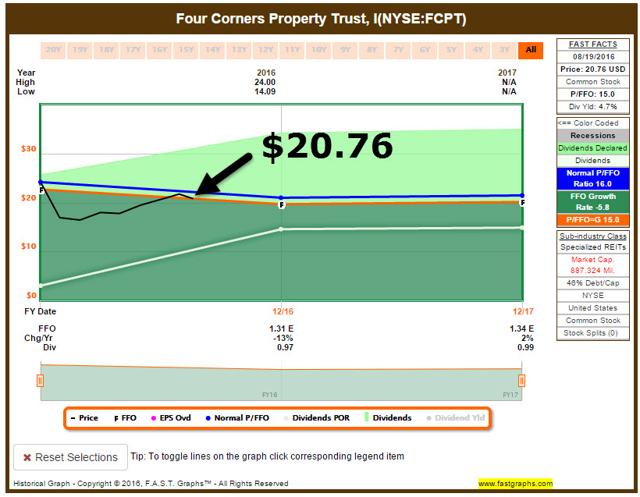

Now let’s compare the P/FFO multiples below:

Source: S&P Global Market Intelligence

Since my last article on FCPT, there has not been a noticeable change, other than a continued flight to income. We suspect that FCPT will continue to trade at a premium until rates increase, at such time we expect a pullback in all Net Lease REITs.

In conclusion, we like FCPT because the portfolio is beginning to round out. By adding new tenants, we believe the company can become a more diverse net lease REIT. However, in our view, investors are not being compensated adequately for the risk and we will wait for a better entry price. Four Corners Is Becoming More Round But The Price Is Not Sound.

Author’s Note: Brad Thomas is a Wall Street writer, and that means he is not always right with his predictions or recommendations. That also applies to his grammar. Please excuse any typos, and I assure you that he will do his best to correct any errors if they are overlooked.

Finally, this article is free, and the sole purpose for writing it is to assist with research (Thomas is the editor of a newsletter, Forbes Real Estate Investor), while also providing a forum for second-level thinking. If you have not followed him, please take 5 seconds and click his name above (top of the page).

Sources: FAST Graphs, FCPT Q2 Supplemental, and S&P Global Market Intelligence.

Disclaimer: This article is intended to provide information to interested parties. As I have no knowledge of individual investor circumstances, goals and/or portfolio concentration or diversification, readers are expected to complete their own due diligence before purchasing any stocks mentioned or recommended.

Disclosure: I am/we are long O, DLR, VTR, HTA , STAG, GPT, ROIC, HCN, OHI, LXP, KIM, WPC, DOC, EXR, MYCC, TCO, SKT, UBA, STWD, CONE, BRX, CLDT, HST, APTS, FPI, CORR, NHI, CCP, CTRE, WPG, KRG, SNR, LADR, PEB, BXMT, IRM, CIO, LTC.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.