High Dividend Stock Yields 11%, Pays Monthly, Goes Ex-Dividend This Week

We went back on the monthly high dividend payers trail, where our recent articles have portrayed quite a few stocks which could smooth out your cash flow.

We first uncovered DirectCash Payments, Inc., (OTC:DCTFF), about 3 months ago. DCTFF is one of the largest branded ATM providers in Canada and Australia, and the third largest branded ATM provider in the United Kingdom. This article will update the information about the company that we covered in that 1st article. (All $ amounts are in Canadian currency, except where otherwise noted).

This Canadian stock trades on the Toronto Exchange, under the ticker DCI.TO, and also on the OTC market in the US. The “F” at the end of its US OTC DCTFF ticker means that it is fungible and can be bought and sold interchangeably on both markets. As with most foreign stocks, it can give you some diversification from US assets.

The company IPO’d in late 2004, and has paid monthly dividends consistently since then, with a 192% total return since then.

They’ve paid $.12/share monthly since August 2014, but, due to currency fluctuations between the Canadian loonie and the US dollar, your payouts will vary a bit from month to month.

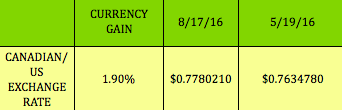

Currently, the loonie has actually gained just under 2% vs. the $, since our initial article came out 3 months ago, so DCTFF’s payouts have inched up slightly.

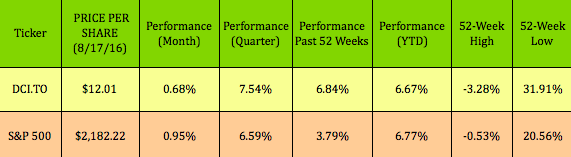

The currency bump has helped its shares to have price gains of around 7.5% over the past quarter:

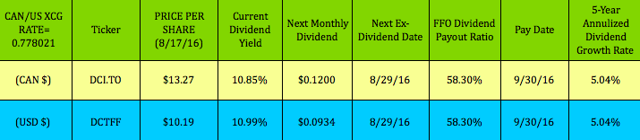

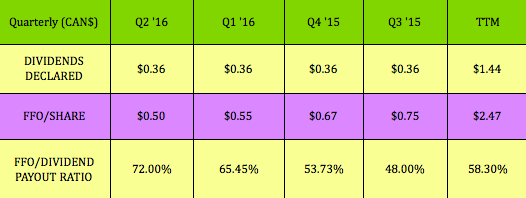

Dividends: This table lists the dividend payouts for both the Toronto-based DCI.TO shares, (in Canadian $), and the US-based OTC shares, (in USD$).

Although it doesn’t go ex-dividend until Monday, 8/29/16, you’d have to own shares this week, to be eligible for the next monthly payout.

Our High Dividend Stocks By Sector Tables track DCTFF’s price and current dividend yield (in the Consumer Discretionary section).

The company’s policy is to pay dividends on or about the last day of each month to shareholders of record on the last business day of the preceding month.

Options: There are no call or put options available for DCTFF, but you can see details for over 30 other income-producing trades in both our Covered Calls Table and our Cash Secured Puts Table.

Earnings: In Q2 2016, the company spent a larger than normal amount on maintenance of its ATM machines, which management characterized as “Extraordinarily lumpy maintenance capital as it relates to EMV upgrades in Australia”. (Source: DC website)

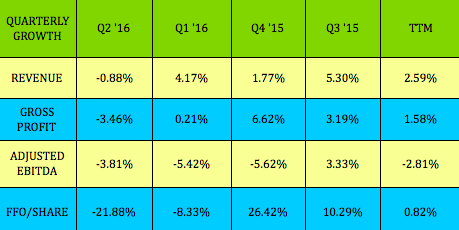

As a result, its FFO/share, EBITDA, Gross Profit, and Revenue all dipped for the quarter:

This caused its FFO/Dividend Payout Ratio to move higher also, continuing a negative trend from the past 3 quarters. Its trailing payout ratio is now 58.30%, vs. the previous rate of 55.17% from 3 months ago – higher, but not drastically so:

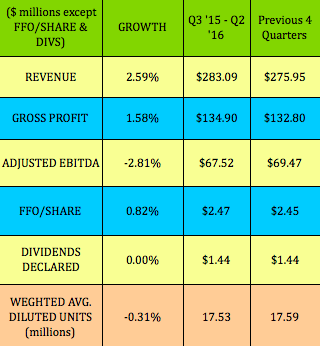

Over the past 4 quarters, the company’s revenues, gross profit, and FFO/share have had some growth, while its EBITDA slipped -2.81%. Dividends have been steady, and they’ve decreased the share count slightly:

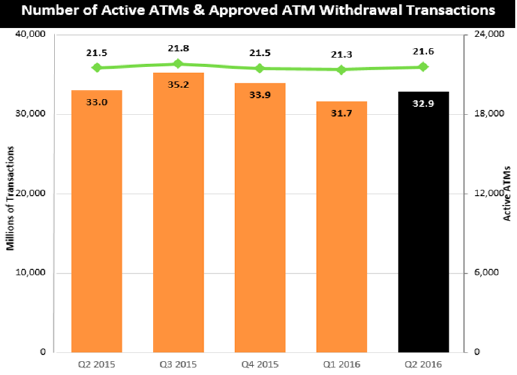

ATM counts and transactions both climbed in Q2 vs. Q1 2016:

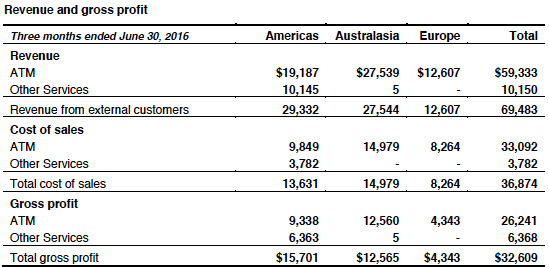

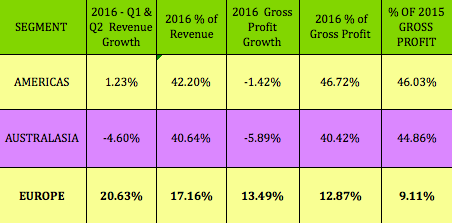

Here’s the geographical segment breakdown for revenues and gross profits for Q2:

(Source: DC website)

For the 1st 6 months of 2016, their revenue actually jumped over 20%, and their gross profit rose over 13%, in Europe. Australasia was the weakest area, with revenue falling -4.6%, and gross profit falling -5.89%:

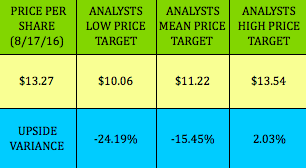

Analysts’ Targets: Analysts’ targets have remained pretty steady over the past 3 months – the mean target was $11.46, and has eased down to $11.22. The shares are now just 2% below the high price target of $13.54. Given the thirst for yield in 2016, and, in particular, monthly dividends, this isn’t surprising.

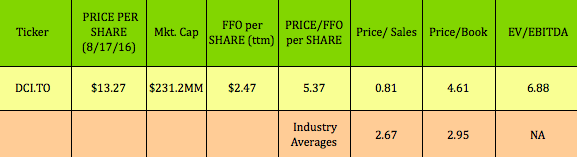

Valuations: The company’s Price/FFO per share and EV/EBITDA still look lower than many other valuations we’ve seen in 2016. It looks cheaper than broad industry averages on a Price/Sales basis, but is commanding a premium Price/Book valuation.

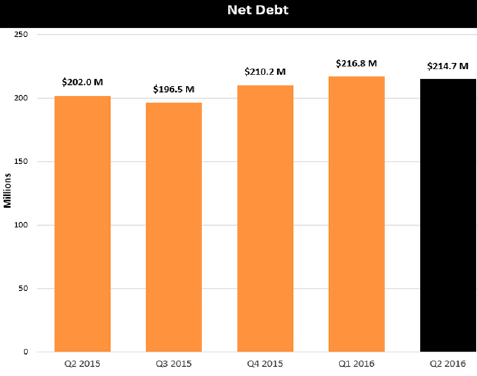

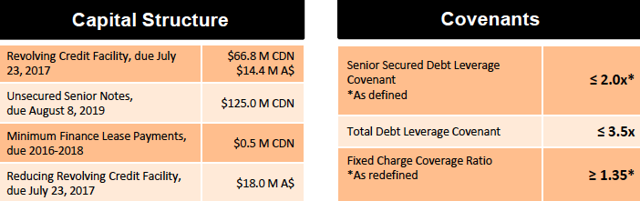

Debt & Capital Structure: Their net debt inched down by 1% in Q2 2016.

The company’s current 2x Debt Leverage ratio is well below its total debt leverage covenant limit of 3.5x. Its largest debt commitment, $125mm of unsecured notes, doesn’t mature until 2019:

(Source: DC website)

All tables furnished by DoubleDividendStocks.com, unless otherwise noted.

Disclaimer: This article was written for informational purposes only, and isn’t intended as personal investment advice. Please practice due diligence before investing in any investment vehicle mentioned in this article.

Disclosure: I am/we are long DCTFF.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.