Nutanix Is A Unicorn Getting Ready To Fly Its IPO

Nutanix (Private:NTNX) is a high growth datacenter virtualization software “unicorn” getting ready for an IPO.

The company has strong revenue growth rates, tremendous customer loyalty and upsell and improving gross margins.

With a previous private market valuation of $2 billion, an IPO valuation near that range should be one worth your serious consideration.

Company Background

San Jose, California-based Nutanix integrates server and storage resources inside the datacenter to help enterprises streamline and simplify their IT infrastructure operations.

The 1,800 employee company was founded in 2009 by IT and storage industry veterans, current CEO Dheeraj Pandey and co-founders Ajeet Singh and Mohit Aron. Pandey was previously from Aster Data and before that Oracle (NYSE:ORCL), where he managed development of the storage engine for the Oracle Database and Exadata products.

(Source: Nutanix YouTube)

Nutanix’ business model assumption is that data centers of the future will run on commoditized x86 blades and that the differentiating factors in capabilities will be in the virtualized software-defined platforms that will span public, private and hybrid cloud environments. This “software-defined, commodity hardware” approach was popularized by cloud behemoth Google (NASDAQ:GOOG)(NASDAQ:GOOGL).

Technology

Nutanix has two primary product families: Prism and Acropolis.

- Prism provides enterprises with virtualization and infrastructure management in a single integrated package that features what the company calls “one-click administration capabilities” based on company-specific rules automation.

- Acropolis delivers distributed storage, mobility capabilities and a built-in hypervisor which enables companies to have multiple operating systems running on a single hardware host.

The company’s solutions can be delivered either as software only or as an on-premise appliance that is configured to the customer’s specifications.

Nutanix stated in its recent S-1/A filing that it had 3,100 “end-customers as of April 30, 2016, including approximately 285 Global 2000 enterprises.”

Competition

Nutanix operates in what Gartner calls the “integrated systems” segment of the IT infrastructure market. It divides its competition into three categories:

- Software providers – VMware (NYSE:VMW) and Red Hat who provide virtualization and related products

- Traditional IT providers – HPE (NYSE:HPE), Cisco (NASDAQ:CSCO), Lenovo, Dell, Hitachi and IBM (NYSE:IBM) that offer integrated systems

- Traditional storage vendors- EMC (NYSE:EMC), NetApp (NASDAQ:NTAP) and Hitachi Data Systems

So the company is competing against extremely large players who have deep pockets and established customer bases from which to innovate in software and services environments.

Financials

For the nine months ended April 30, 2016, Nutanix reported revenues of $305 million vs. $167 million in the same period in 2015, representing a whopping Year-over-Year growth rate of 83%.

2015 vs. 2014 revenues showed a YoY growth rate of 90%, so growth rates are slowing somewhat. This slowing growth rate is not uncommon for enterprise software companies such as Nutanix, but is nevertheless something to watch.

Gross margin was 62% in the most recent nine-month period vs. 58% during the same period in 2015, representing a meaningful improvement.

Nutanix had $192 million in cash on hand as of April 30, 2016.

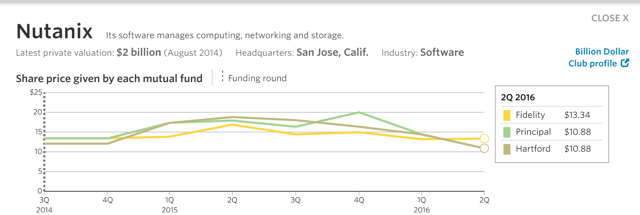

The company’s most recent private market valuation was reported as $2 billion, as of its most recent funding round of $140 million in August, 2014.

(Source: WSJ Online)

IPO Opinion

Assuming moderate market volatility, Nutanix will likely IPO soon and perform well. Reports are that the buy side of the market is hungry for new issues, especially after the recent market doldrums of the Brexit event and the approaching end of summer.

Although the IPO market has been largely devoid of non-life science offerings, recent IPOs of software companies such as Twilio (NYSE:TWLO) and Line (Pending:LN) have performed well, whether accompanied by an opening day rise by Twilio, or an initial drop and subsequent rise in Line’s case.

Both of those IPOs were for companies with large revenue run rates and very strong revenue growth comparables, both important features that Nutanix shares.

The company also cites an 80% upsell rate for its customers of 18 months or more, which indicates tremendous customer satisfaction and loyalty.

I’m quite bullish on Nutanix as an IPO candidate, since it has a strong financial position, excellent growth and loyalty rates and improving gross margins even as it continues to invest in its sales and marketing efforts for further market share growth.

From here, Nutanix is a sales and marketing play in the medium term, offering its integrated cloud management solutions for the middle market enterprise, a market with strong future growth rates.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.