Two Harbors Investment Corp. Provides Clarity

A preview of this article was provided to subscribers on 08/17/2016.

Two Harbors Investment Corp. (NYSE:TWO) announced their decision to leave the mortgage loan and securitization business. They are still a mortgage REIT, but they decided to leave one niche in the market so they could simplify their presentations and invest capital in more efficient uses. That simplification is supported by management’s notes in the 10-Q:

“Note 23. Subsequent Events

On July 28, 2016, the Company announced that its board of directors had approved a plan to discontinue the Company’s mortgage loan conduit and securitization business. This decision was made due to the challenging market environment facing the business, combined with the intent to reduce operating complexity and costs, and will allow for the reallocation of capital to more attractive and efficient target assets. The wind down process is expected to be substantially completed by the end of 2016.”

That simple explanation of their intent should give shareholders a better understanding of what to expect. Given that management is ending the segment due to a challenging landscape, investors probably shouldn’t expect it to generate incredible returns over the next few months. Fortunately, TWO has a few other segments that are simpler to present, simpler to analyze, and as management indicated, the other segments have “more efficient target assets”.

TWO’s Comments Were Brutal

Management did more than state that they were concerned about asset performance. They referred to the “challenging market environment facing the business”. This is a decision made over the summer. Chimera Investment Corporation (NYSE:CIM) uses the conduit model heavily in their business. They have been rallying to highs while one of the largest mortgage REITs came forward and stated that the business model faces challenging conditions.

I will put together some more work specifically on CIM.

Implications for TWO

Two Harbors Investment Corp. may see some short-term cost recognition, but they will probably adjust non-GAAP metrics accordingly. I don’t foresee the short-term costs being a material issue for performance. Guidance from management indicates a one-time cost of around $3 million in the second half followed by annual savings of around $10 million to $11 million.

Over the longer term, this could be a positive factor for the company since a simplification of their structure will further simplify analysis. If we reach a point where mREITs deserve a premium to book value (a steep yield curve and a large MBS to LIBOR spread), clarity in presentation would make it easier to grow the portfolio by keeping a stable share price if management wanted to issue more equity.

I wouldn’t expect them to issue equity until they were trading above, or at least close to, book value.

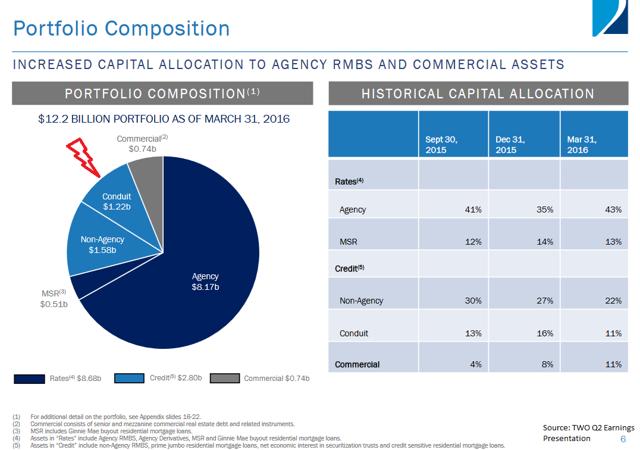

How Big Was the Securitization Business?

The conduit business was making up around 10% of the total investment portfolio. That is a decline relative to the weight of the conduit segment in the winter.

In December, the allocation to the conduit strategy was at a high of 16%. Since then the company has been dialing back their use of the strategy and assets in favor of other areas.

You might be asking:

“Does management see anywhere that there is a particularly strong opportunity for investing?”

To understand where Two Harbors Investment Corp. is going, investors need simply look at where management is more optimistic.

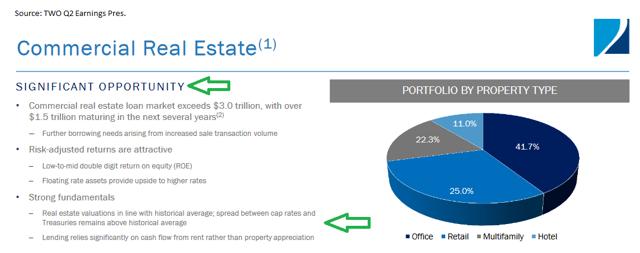

Management identifies commercial real estate as an area with significant opportunity and points to the strong spread between capitalization rates and treasury rates. That is a useful observation because it suggests that the amount of income the landlords are generating from their business should be stronger relative to the size of the payments they have to make.

It would also be worth pointing out that CMBS include protections against prepayments. Because the CMBS are protected from prepayment, their value can increase more significantly when rates move lower. They also fall further if rates decline. The nice thing about the simple structure of a CMBS bond is that the timing of expected cash flows is known. For RMBS, there is a substantial amount of estimation involved. Because CMBS have known cash flows (assuming no default), they can be hedged more effectively with LIBOR swaps.

Remember that LIBOR rates at several durations – especially the longer durations – are lower than treasury rates. That means hedging duration risk through LIBOR swaps is cheaper than it used to be. The 5-year LIBOR swap is running about even with the 5-year treasury now, but the 10-year LIBOR swap is about 13 basis points cheaper than the treasury. For an investor in mortgage REITs, a 13 basis point difference can be significant.

Valuation

This is where things get tricky. TWO was recently trading at 91.35% of trailing book value. The mREIT has been on a clear trend higher, which coincides with the domestic equity markets constantly moving higher. While I like the way TWO is modifying their portfolio, I do not like the high levels of equity markets or the much higher price to book ratios throughout the mREIT sector. Despite the improvements, I have to leave TWO at a neutral rating. It might be worth looking at TWO for a potential play in a pair trade where it could be used to hedge shorting a stock trading at higher multiples. Unhedged exposure to mortgage REITs right now should emphasize mREITs trading at discounts larger than 10%. Preferably, the discount should be materially larger.

Want to Know More About Mortgage REITs and Preferred Shares?

The Mortgage REIT Forum is a new exclusive research platform. My first 100 subscribers will be able to lock in their subscription rates at only $240/year. My investment ideas emphasize finding undervalued mortgage REITs, triple net lease REITs, and preferred shares. With the market at relatively high levels, there is also significant work on finding which securities are overvalued to protect investors from losing a chunk of their portfolio.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Information in this article represents the opinion of the analyst. All statements are represented as opinions, rather than facts, and should not be construed as advice to buy or sell a security. This article is prepared solely for publication on Unique Finance and any reproduction of it on other sites is unauthorized. Ratings of “outperform” and “underperform” reflect the analyst’s estimation of a divergence between the market value for a security and the price that would be appropriate given the potential for risks and returns relative to other securities. The analyst does not know your particular objectives for returns or constraints upon investing. All investors are encouraged to do their own research before making any investment decision. Information is regularly obtained from Yahoo Finance, Google Finance, and SEC Database. If Yahoo, Google, or the SEC database contained faulty or old information it could be incorporated into my analysis. Tipranks: Assign no ratings.