AIG’s United Guaranty Sale, By The Numbers

On August 15, 2016, American International Group (NYSE:AIG) announced that the company entered into an agreement to sell its 100% interest in its subsidiary United Guaranty to Arch Capital Group Ltd. (NASDAQ:ACGL) for total consideration of $3.4b. The $3.4b total consideration consists of $2.2b of cash, $250m of preferred stock, and $975m of convertible common-equivalent preferred stock.

In addition to the total consideration, AIG disclosed the retention of a block of business:

“…AIG will retain all mortgage insurance business ceded under an existing 50% quota share agreement between UGC and AIG subsidiaries for business originated from 2014 through 2016. “

Earlier in the year, AIG announced intentions of spinning off a portion of United Guaranty (under 20%) and there were rumors (for example, see this report) that the company was seeking a $4b valuation for its subsidiary. Therefore, at first glance, AIG appears to be on the short-end of this deal but there are a few other factors that must be considered before coming to a final conclusion.

First, investors must remember that management’s long-term goal is to create a “leaner, more profitable and focused insurer” and that the United Guaranty sale is in line with this strategy. Second, it is hard, or should I say impossible, to put an exact dollar figure on the business that AIG will retain from United Guaranty but there is undeniably some value to keeping a block of business of a growing and profitable subsidiary. Lastly, the “other” consideration (i.e. preferred stock and convertible preferred stock) has some upside potential that could create a lot of value for AIG over time if this sale is beneficial to Arch’s business in the quarters/years ahead.

(Image Source)

My intention within this article is not to try to convince investors that AIG got the better end of the deal, but instead, I want to take a deeper dive into the numbers to determine if AIG received what I would consider a fair price for the sale of its subsidiary.

Did AIG Receive A Fair Price For The Sale of United Guaranty?

In order to determine if AIG received a fair price for United Guaranty (aka “Mortgage Guaranty”), I took a deeper dive into the most recent quarterly reports (10-Q and earnings press release) and the company’s annual report (10-K).

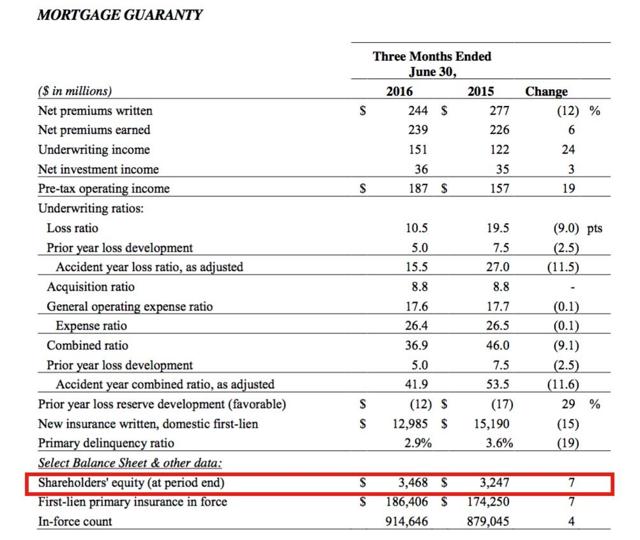

To start, Mortgage Guaranty had shareholders’ equity of ~$3.4b at the end of June 30, 2016.

(Source: AIG’s Q2 2016 Earnings Press Release)

Therefore, AIG will receive ~1x book for the sale of its subsidiary and this is without taking into consideration the retained business or the potential upside for the other consideration. Without going any further, this shows that AIG received a slight premium for the business but let’s take it a step further by comparing this to the valuation that the Radian Group (NYSE:RDN), widely viewed as Mortgage Guaranty’s closest competitor, is currently receiving in the market.

RDN Price to Book Value data by YCharts

As shown, Radian is currently trading around 1x book, so, in my opinion, AIG will receive what should be considered a fair price for the subsidiary.

However, let’s now take a look at the subsidiary’s prior operating results to determine if AIG is selling a business that is struggling from an operational standpoint.

| Six Months Ended June 30, | ||

| ($ in millions) | 2016 | 2015 |

| Underwriting income | $278 | $233 |

| % chg | 19% | |

| Net investment income | $72 | $69 |

| % chg | 4% | |

| Pre-tax operating income | $350 | $302 |

| % chg | 16% | |

| AIG’s consolidated pre-tax operating income | $2,574 | $5,395 |

| MG’s pre-tax operating income as % of consolidated pre-tax operating income | 14% | 6% |

| KEY METRICS: | ||

| Combined ratio | 41.7% | 50.9% |

| % chg | (18)% | |

| 60+ day delinquency ratio on primary loans | 2.9% | 3.6% |

| % chg | (19)% | |

(Source: Data from AIG’s 10-Q for period ended June 30, 2016; table created by W.G. Investment Research)

As shown, Mortgage Guaranty’s operating results over the first half of 2016 have significantly improved when compared to the first six months of 2015. Mortgage Guaranty’s pre-tax operating income is up ~16% YoY, and the subsidiary’s income now accounts for ~14% of AIG’s total consolidated pre-tax operating income.

Moreover, Mortgage Guaranty has reported improving operating results over the last three fiscal years.

| ($ in millions) | 2015 | 2014 | 2013 |

| Underwriting income | $505 | $454 | $73 |

| % chg | 11% | 522% | |

| Net investment income | $139 | $138 | $132 |

| % chg | 1% | 5% | |

| Pre-tax operating income | $644 | $597 | $205 |

| % chg | 8% | 191% | |

| AIG’s consolidated pre-tax operating income | $4,055 | $9,574 | $9,390 |

| MG’s pre-tax operating income as % of consolidated pre-tax operating income | 16% | 6% | 2% |

| KEY METRICS: | |||

| Combined ratio | 44.6% | 52.6% | 91.1% |

| % chg | (15)% | (42)% | |

| 60+ day delinquency ratio on primary loans | 3.4% | 4.4% | 5.9% |

| % chg | (23)% | (25)% |

(Source: Data from AIG’s 10-K for fiscal year ended December 31, 2015; table created by W.G. Investment Research)

Observations from the tables:

- Mortgage Guaranty has become more and more important to AIG’s bottom line, as the subsidiary went from accounting for ~6% of the company’s consolidated pre-tax operating income in 2014 to now accounting for over 10%.

- The combined ratio has significantly improved over the years and the ratio is now under 45%

- The 60+ day delinquency ratio is trending in the right direction

There is no denying that the Mortgage Guaranty subsidiary is a growing business, but, in my opinion, management made a prudent decision in selling the division outright instead of devoting the time to spinning off a portion of the subsidiary and retaining a large stake in a non-core business. Additionally, AIG may be selling Mortgage Guaranty at an opportunistic time due to the improving operating results over the past few years and the likelihood that this type of growth will be harder to come by in 2017 and beyond.

The most important takeaway is that management made a decision that is line with their previously communicated strategy of streamlining the business and focusing on the core operations, specifically Property Casualty, while also being able to receive a fair price for the sale. It should also be noted that the Mortgage Guaranty business now appears to be more important to AIG’s bottom line due to fact that the company’s consolidated pre-tax operating income is being negatively impacted by the challenging operating environment –i.e. low interest rate environment (as shown by the trending of the pre-tax operating income in the tables above).

The End Result, Buybacks

Management intents to return ~$25b to shareholders over the next few years, so the Mortgage Guaranty deal will definitely put AIG in a stronger position to meet this lofty goal. To illustrate how this deal may impact future buybacks, I used a more realistic figure ($2b) instead of $3.4b because AIG is only expected to receive $2.2b in cash from Arch.

| Shares outstanding* | 1,070,659,944 | |

| Potential Buyback ($) | $2,000,000,000 | |

| Share Price @ 8/19/16** | $58.76 | |

| Potential Buyback (shares) | 34,036,760 | |

| Shares outstanding after potential buyback | 1,036,623,184 | |

*Per 10-Q for period ended June 30, 2016 –linked above

**Per Yahoo! Finance

In this scenario, AIG would be able to reduce the share count by ~3%. If the total consideration of $3.4b was used in the calculation, AIG would reduce the share count by ~5%.

This company has already spent ~$6.9b so far in 2016 to buyback shares so the potential buyback from this sale will be in addition to the already anticipated buybacks.

Bottom Line

The United Guaranty, or Mortgage Guaranty, subsidiary has great long-term business prospects in place and Arch’s operations will likely greatly benefit from this transaction, but, in my opinion, AIG’s management team made a great decision to sell a non-core business at an opportunistic time while also receiving what I would consider to be a fair price. Thinking ahead, I agree with Mr. Carl Icahn that AIG should continue to sell non-core businesses and use the proceeds to fund buybacks.

Investors should not run out tomorrow to purchase AIG shares, but, as I describe in this article, any significant pullback should be considered a buying opportunity because shares are attractively valued and should be trading in the mid-$60’s over the next 12-18 months.

Full Disclosure: I own AIG shares and warrants in my R.I.P. Portfolio, and I recently added to my position.

If you found this article to be informative and would like to hear more about this company, or any other company that I analyze, please consider hitting the “Follow” button above.

Disclaimer: This article is not a recommendation to buy or sell any stock mentioned. These are only my personal opinions. Every investor must do his/her own due diligence before making any investment decision.

Disclosure: I am/we are long AIG.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Stock Plaza). I have no business relationship with any company whose stock is mentioned in this article.