Alliance Data Systems: If You Don’t Like The Answer, Just Change The Question

Citron Target on Alliance Data Systems Corp is 50% Near-Term Downside

This month Citron Research celebrates its 15th year of publication – exposing, for lack of a better term, “market inefficiencies.” This neutral-sounding moniker is occasionally an accident… but rarely. Most often it exploits the shallowness of Wall Street’s “insight” wit management’s intentional hype, misdirection or just plain fraud. It has become too profitable taking advantage of a bullish market environment to ever let the truth get in the way of a good story.

And then comes Citron Research.

In the case of Alliance Data Systems (NYSE:ADS), Wall Street is just now waking up to the misrepresentations that have been promulgated by ADS management. At best, this is a mis-categorized company which should immediately be priced 40% lower. At worst management is covering up a business that has an entirely different risk profile… and is one big credit event from derailing into a devastating downward spiral.

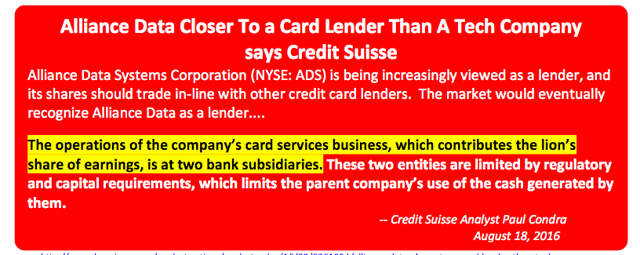

What makes this story timely is that it is not just Citron but Wall Street analysts who are finally catching up to the story, as reflected in this week’s note from Credit Suisse, which states:

Source

Citron could not have said it better. However, although Credit Suisse did acknowledge the elephant in the room, they stopped short of driving their verdict to its inevitable valuation conclusion.

“Increasingly Viewed As A Lender”

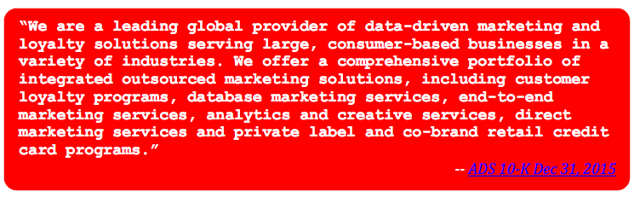

Let’s begin with the background for those who are not familiar with Alliance Data Systems. This is what management claims they do in their most recent 10-K:

Source

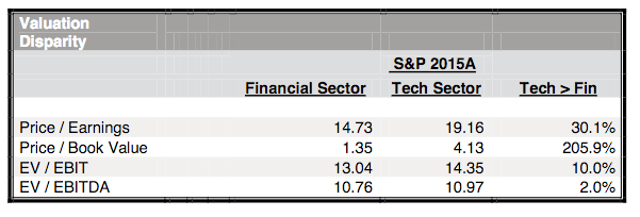

This would lead most investors, and importantly, indexers, to categorize ADS as a business services company, which deservedly trades on earnings rather than book value, and be assigned a higher multiple than a bank.

But as Credit Suisse noted, the lion’s share of earnings do in fact come from the banks they operate. The myth of ADS being a business services company has been widely accepted because the company is in the S&P 500 Information Technology Sector Index but not the S&P 500 Financial Sector Index. Alliance Data Systems has no incentive to correct this obvious mis-categorization – management prefers the higher valuations that are associated with tech companies.

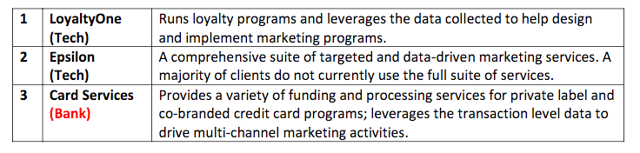

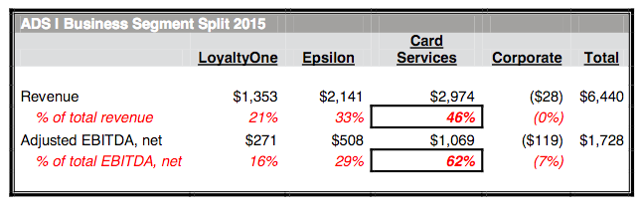

Three divisions of ADS must be considered separately when valuing the company:

So while LoyaltyOne and Epsilon can fairly be valued as members of the Business Services (NYSE:IT) cohort, ADS is more and more a bank wrapped in the Halloween costume of a business services company.

The Obvious Next Question: What’s The Breakdown?

As we can see, “Card Services” are more often than not discussed last, but is by far the most important division of Alliance Data Systems. The bank – like portion of the business, is almost two-thirds of the business. From the chart below you can see why ADS would rather be considered a tech services firm than a bank:

There aren’t too many tech companies out there that report zero Research and Development costs… but it gets even more obvious than that.

What Does Alliance Data Systems Really Do? Numbers Don’t Lie!

The majority of its income being generated from its banks, ADS is clearly not primarily a technology company. As the operator of Comenity Bank, ADS issues credit cards from Victoria Secret, JCrew, Ulta, and a list of other retailers.

For those who defend the company claiming it should trade at a premium because their might be synergies between the two business … this is simply untrue. Citron’s investigation makes clear that the crossover between clients is statistically insignificant; instances can be counted on one hand. The only ones of note are Express and New York & Co.

Management Has Promoted This Deception

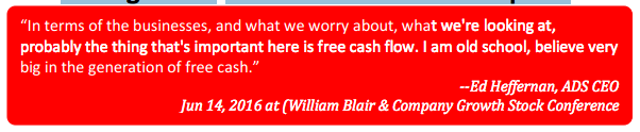

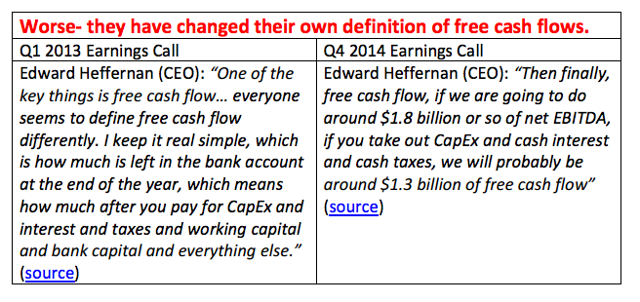

Meanwhile, the company stopped reporting free cash flow in its Q2 2016 investor presentation (the last time it was not disclosed was Q4 2014).

Generation of free cash is NOT what a bank should be focused on.

More importantly the company is categorized into the Info Tech part of the S&P Index. (see here)

Worse, ADS is explicitly in the “S&P 500 Ex-Financials” Index

Yet, until now analyst have still been complacent spouting off free cash flow when discussing the financial health. Almost like having a conference call about how fast Usain Bolt can swim: WHO REALLY CARES…?

Plain and Simple:

ADS sells the investment community on cash flows, not return on equity or return on assets, metrics that a bank would be valued on. Instead they refer to financial metrics that are akin to a technology company.

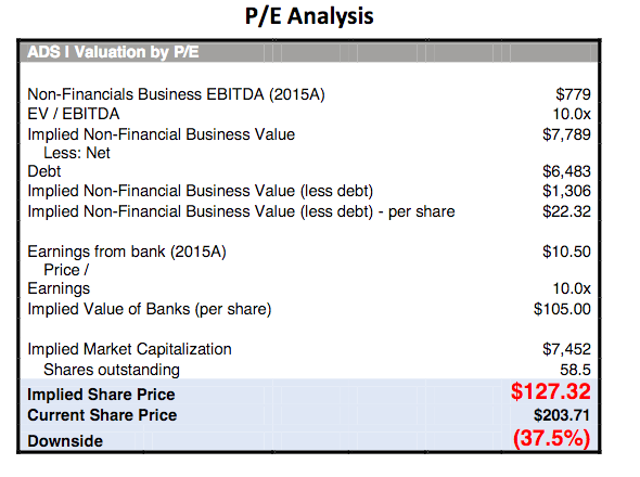

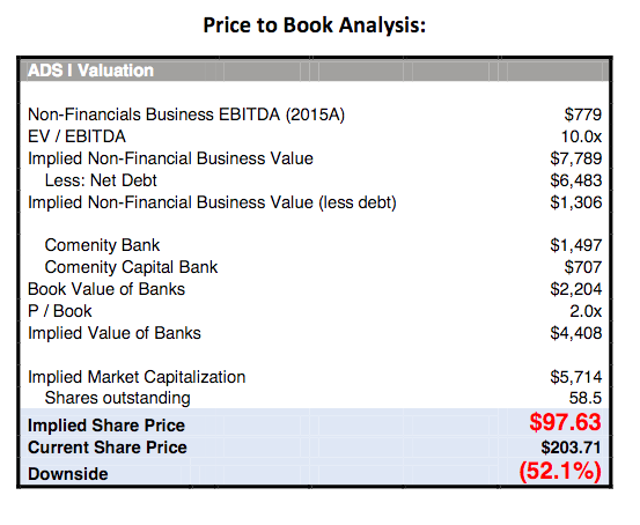

The Only Intellectually Honest Way To Value ADS

While Credit Suisse got the ball rolling… Citron now completes and publishes the obviously needed analysis. Because of its two completely different business units, the only way to value ADS is a complete sum of the parts analysis – looking at the bank and the tech operation separately. To be fair, we assign the non-bank business a fair multiple of 10x EBIDTA, which is widely accepted for this type of business. This is right in line with Amiya (AIM in Toronto), the largest of all customer loyalty data driven companies. We will add that to the value of the banks, assigning them a 2x book value, which is the same as Synchrony Financial, the gold standard of private label credit cards.

*NOTE: The corporate debt must be assigned to the loyalty business. Due to Section 23 of the Federal Reserve Banking Regs, banks cannot hold corporate debt. They certainly can’t raise debt to buy back shares. This concern is acknowledged in the GS research report on ADS.

Because its more than half a bank, not a tech firm, the valuation models of Alliance are miles from reality!

Realigning Perceptions and Reality

In a best-case scenario, ADS should trade at $100 per share – $125 tops – which is more than fair. Worst case scenario, it could go much lower with a credit event. While this story does need to explain what could happen, investors would be foolish not to pay attention to a lender with more red flags than the Beijing Olympics… all which could trigger a credit event and send the stock lower than our projections.

The Single Most Disturbing Data Point About ADS:

ADS DOES NOT disclose FICO scores of their borrowers. They are the only credit company in the S&P 500 that does not… this is beyond disturbing, because they intentionally cater to a lower than prime client. See the “Shopping Cart Trick” below.

And the Other Red Flags:

- Many of ADS private label credit cards purposely do not offer an auto pay feature, which enables them to earn a higher ROE from late fees charged. This has already been the target of the FDIC and could go to the CFPB.

- Comenity bank already has history of run-ins with regulators, and has been fined. CFPB is always a threat. (here)

- ADS is possibly the only bank on the S&P 500 that does not disclose return on equity or return on assets.

- ADS is the rare financial institution on the S&P 500 that has > $5 billion of debt and no credit rating.

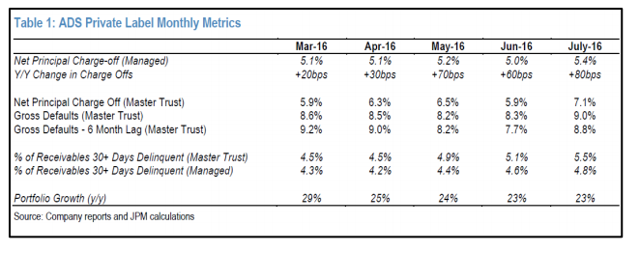

- The sub-prime book is becoming more apparent – you can see the connection to Lending Club of page 9 of their most recent 10-K.

Charge-offs are growing:

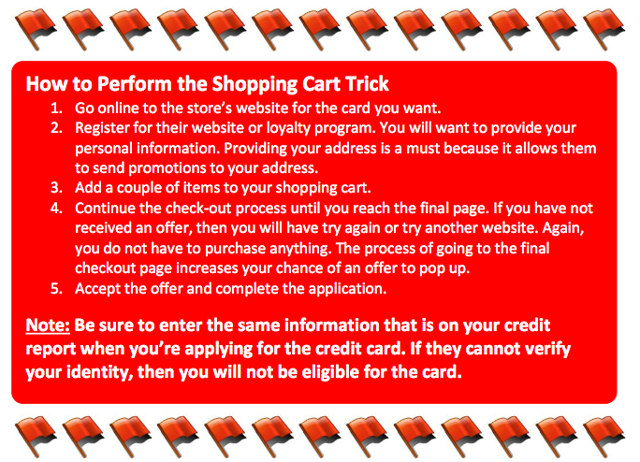

Lastly, and the Biggest Red Flag of them All, is Comenity’s Prominent Use of the “Shopping Cart Trick”

Citron believes that a big part of the online credit card business of Comenity is based on a widely known trick among the subprime community which allows consumers to get credit, especially high fee retail-branded credit cards, without a credit request ever getting put on your credit records or lowering your FICO score. Comenity is well aware of this credit loophole – you will be amazed of how popular it has become with the subprime community. Below are just three but there are literally hundreds of sites and videos dedicated to this Comenity “loophole.” Folks this is the Holy Grail of subprime lending:

(Source)

Other links documenting the same nonsensical sleight-of-hand – an engraved invitation to subprime customers – here and here.

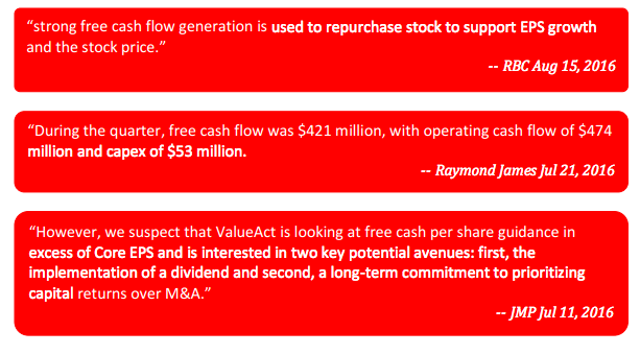

So Why Do Investors Own ADS?

Simple: Investors buy ADS as a yield name as it boasts 10% free cash flow yields. Yet, using this metric for a bank instead of its price to book is like asking Ryan Lochte how his night was. You’ll get an answer; it’s just that reality might be a different story.

The company has said numerous times in SEC filings that in 2015 they generated $1.3 billion in free cash flow. This is not only misleading – in our opinion this is borderline fraudulent.

In a time where we all increasingly struggle to understand or delineate GAAP vs. non-GAAP figures, the SEC has attempted to add clarity with Regulation G. This regulation forces companies to “show their homework” when disclosing any non-GAAP financial measures, in this case when disclosing cash flows – Alliance Data Systems should show investors how they were calculated. They should provide a reconciliation of free cash flow to provided GAAP figures (as free cash flow is a non-GAAP figure). But Alliance Data Systems does not do this.

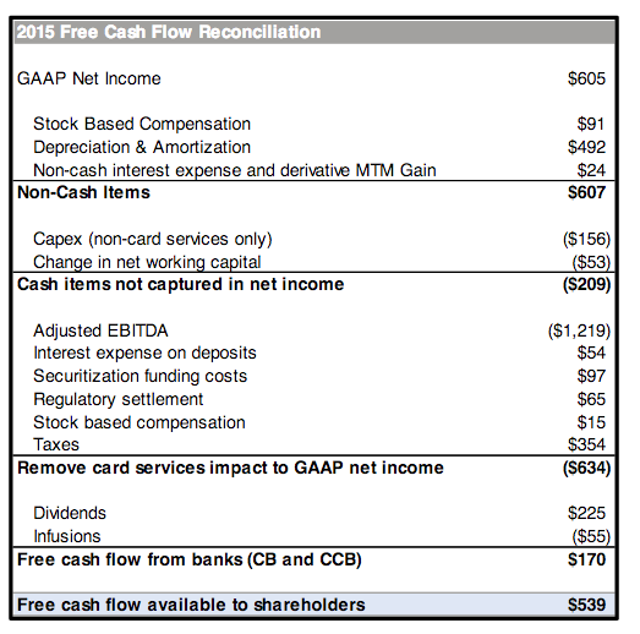

Research done by numerous accountant and industry experts has concluded that the actual free cash flow of ADS is less than half of what is disclosed, just $539 million … and here is the homework.

While ADS wants investors to believe that free cash flow = EBITDA less taxes, capex, interest – in reality and in their own former calculation it is… Net dividends from the two banks to the parent plus the free cash flow of the non bank businesses.

DUH!!!

Everyone knows that EBITDA is the most useless metric when looking at a bank … everyone except maybe ADS.

Conclusion

Citron has attempted to present this story as simply as possible. Goldman Sachs already understands the mispricing of ADS, and reports even its Sum of The Parts analysis is significantly lower than the stock’s current lofty levels. Now Credit Suisse is on board. Pretty soon, all of Wall Street will wake up and understand that at best – Alliance Data Systems is a $100 stock. And if we see a recession or other threat to consumer credit default rates, the floor becomes the ceiling … overnight.

Disclosure: I am/we are short ADS.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.