Alpha From Equal-Weighting: A Look At Materials

In this ongoing series comparing the returns of the capitalization-weighted and equal-weighted sector funds, we have seen outperformance in equal-weighted Financials (+2.97% per year for over ten years), equal-weighted Healthcare (+2.66%), and equal-weighted Consumer Staples (+1.80%). This article will take a look at the Materials sector.

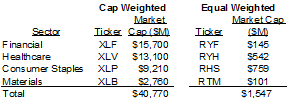

Why is this outperformance notable? As tabled below, there is 26x times as much money allocated to the cap-weighted sector funds I have covered in this series as the equal-weighted sector funds. I understand the attraction of Unique Finance readers to strategic industry tilts, but I want to highlight the potential for greater gains in an oft-overlooked alternative weighting schema.

A Case for Equal-Weighting

In addition to the first three industries we have studied, I have written extensively about the outperformance available through equal-weighting. Check out the articles linked below for further background on the strategy:

- Equal-weighting is one of my 5 factor tilts that have historically outperformed the market;

- Equal-weighting has outperformed in the longest available dataset for the domestic equity market;

- A combination of equal-weighting RSP and the Dividend Aristocrats (NOBL; SDY) has bested the market for fourteen of the last sixteen years.

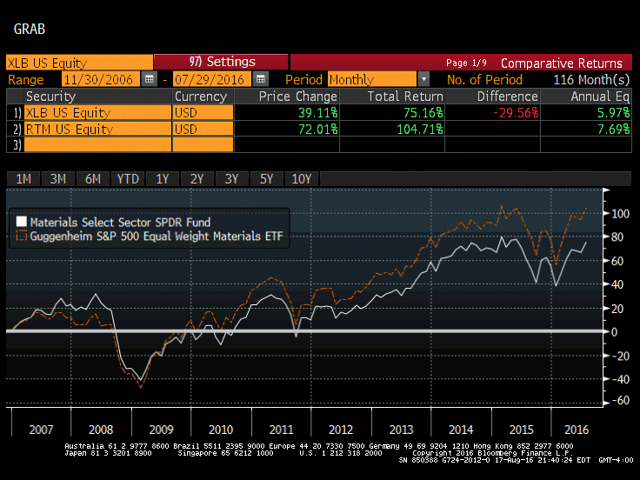

With this voluminous supporting evidence, equal-weighting the Materials sector has also outperformed the capitalization-weighted index over this time period. The total returns of the two exchange-traded funds replicating these indices is shown below. Equal-weighting (RTM; +7.69%) has bested capitalization-weighting (XLB; +5.97%) by 172bp per annum, which translates into a cumulative total return nearly 40% higher. The data dates to the inception of the equal-weighted funds in 2006.

Source: Bloomberg

It is easy to understand why equal-weighting outperformed in Consumer Staples and Healthcare. Those two sectors have strongly outperformed the market over this time horizon, and equal-weighting does well in bull market environments, as the strategy captures a size premium. Materials stocks have not fared as well in recent periods, but this was not enough to derail the overall outperformance of equal-weighting. Equal-weighting actually outperformed in a rocky 2015 for commodity-sensitive companies, besting the return of cap-weighting (-7.89% versus -8.65%).

For the longer time horizon, there have been some idiosyncratic elements that have caused the cap-weighted fund to lag. If you go back to the end of 2006, Alcoa (NYSE:AA), Freeport-McMoRan (NYSE:FCX), and Newmont Mining (NYSE:NEM) were the third, fourth, and fifth largest constituents, respectively, of the Materials sector. In the equal-weighted index, these issuers made up just 1/29th of the fund.

These three companies are the only current constituents of the Materials index which have produced negative cumulative returns over the last decade. Alcoa, which has faced pressure from low-cost Chinese production that caused a global imbalance and depressed prices, has produced a -8.4% total return over the last ten years. Leveraging transactions on the part of Freeport-McMoRan and an ill-timed entry into energy markets has stressed the company’s balance sheet in this period of weak commodity prices. This recent downturn has driven a -4.3% total return over this time horizon. Newmont Mining has produced an average total return of -0.1% over the last ten years, as volatility in gold prices driven by tectonic shifts in global monetary policy has led to some ill-timed investment and hedging decisions that crimped shareholder returns.

Conversely, some of the smallest constituents in the capitalization-weighting index at the end of 2006 have produced very strong returns. International Flavors and Fragrances (NYSE:IFF), which manufactures flavors and fragrances for the food, beverage, personal care, and household products industries, has produced a 16% annualized return over the last decade. Ball Corp. (NYSE:BLL) has metal and food canning businesses as well as an aerospace arm. The company has produced 15% annualized returns. Eastman Chemical (NYSE:EMN), an international chemical company which produces coatings, adhesives, fibers, and performance chemicals, has produced 13% annualized returns. These companies were the fourth, fifth, and seventh smallest constituents, respectively, in 2006. Each of the aforementioned three underperforming stocks has more than double the weight of each of these outperforming stocks combined at the outset of this sample period. Capitalization-weighting had higher weights to underperforming metals names and lower weights to outperforming chemical businesses more closely tied to the U.S. consumer.

M&A has also been a positive uplift for some of the smaller constituents that were in the index at the beginning of the sample period. Hercules Inc. (acquired by Ashland (NYSE:ASH) in 2008), Pactiv (acquired by Reynolds in late 2010), Temple-Inland (acquired by International Paper (NYSE:IP)), and Sigma-Aldrich (acquired by Merck KGaA (OTCPK:MKGAF) in 2015) were all small constituents with more heavy weights in the equal-weighting index that benefited from deal premia to improve returns.

In four articles in this series, we have now seen relative outperformance of equal-weighting in the Consumer Staples, Healthcare, Financials, and Materials space over the trailing decade. Materials did not produce the double-digit annual returns of the Consumer Staples and Healthcare industries, but equal-weighting still boosted performance meaningfully. Materials is a heterogeneous sector given the different supply dynamics for global metals and chemicals. The equal-weighted Materials index has benefited from consumer-oriented business lines and heavy doses of M&A. Future articles will examine equal-weighting versus capitalization-weighting in the other five sectors.

Disclaimer: My articles may contain statements and projections that are forward-looking in nature, and therefore, inherently subject to numerous risks, uncertainties, and assumptions. While my articles focus on generating long-term risk-adjusted returns, investment decisions necessarily involve the risk of loss of principal. Individual investor circumstances vary significantly, and information gleaned from my articles should be applied to your own unique investment situation, objectives, risk tolerance, and investment horizon.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Unique Finance). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I am long equal-weighted funds, but do not have specific exposure to the equal-weighted sector funds.